Top 4 Wise Alternatives in Pakistan

As of May 2026, Pakistani-registered Wise accounts do not include a US routing number or ACH account number, so clients cannot send you money the way they would to a standard US account.

This matters because ACH transfer is the default payout method on Upwork and Fiverr. Without ACH details, you cannot receive platform payouts directly. Pakistani users in the Pakistan reddit community have also confirmed that Wise no longer allows new accounts registered with a Pakistani address to access full account features. Users who opened accounts before this restriction still use them, but new registrations may return a "Receiving is not yet allowed" message.

Beyond receiving, Wise income classified as home remittance creates a separate compliance issue. Pakistani freelancers report that income received via Wise carries an FBR code of 0401, meaning it is classified as remittance rather than freelance income. This matters during FBR audits, where a Payment Reconciliation Certificate (PRC) may be demanded. It is not needed to file a return, but failure to produce it during an audit may carry penalties.

For a new Pakistani user who earns remotely, Wise may not be a functional receiving option. The platforms below are.

As of May 2026, to receive USD with a dedicated ACH account as a Pakistani user, 4 platforms cover the full receiving workflow:

- nsave

- ElevatePay,

- Payoneer

- Hawala.

Each fits a different use case, and the breakdown below maps them to yours.

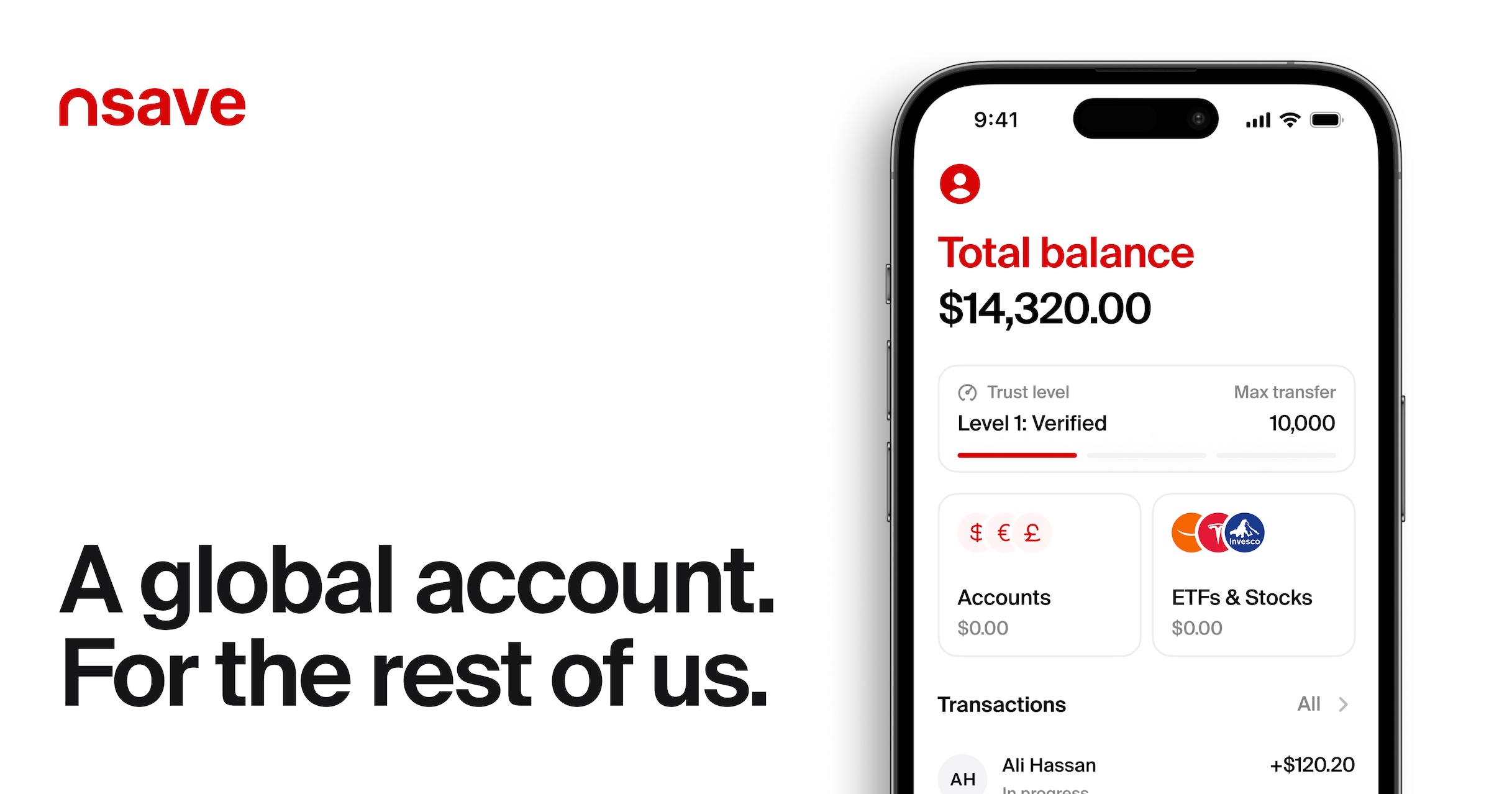

1. nsave

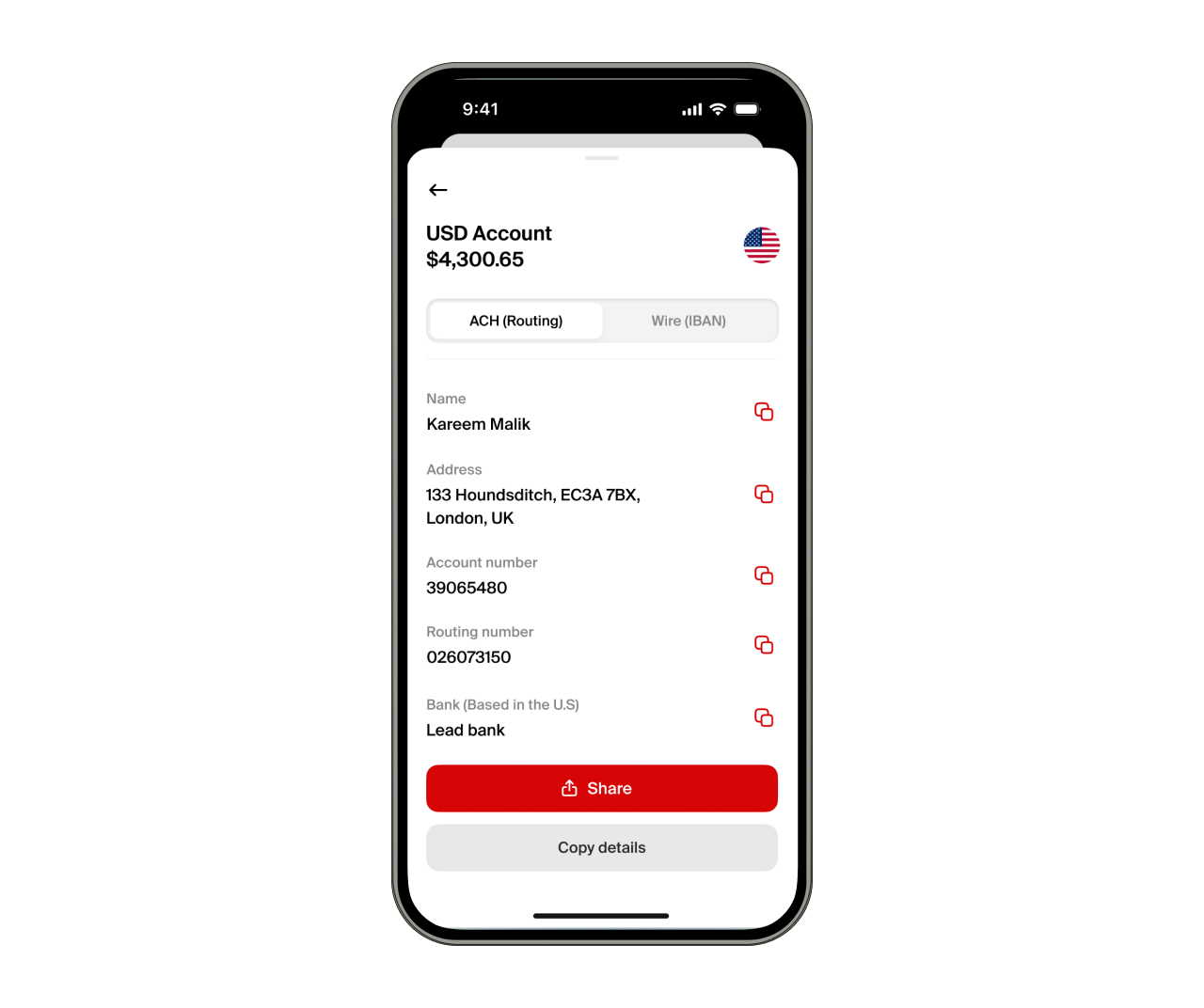

To receive USD payments as a Pakistani user, open a free nsave account. nsave provides a dedicated US routing number and account number for ACH transfers, and accepts inbound SWIFT transfers at no receiving fee.

nsave offers 3 features that matter specifically to Pakistani users:

- Receiving: ACH account details accepted by Upwork, Fiverr, Deel, PeoplePerHour, and direct client transfers. No receiving fee applies to ACH or SWIFT inbound transfers.

- PKR payout: You can convert USD to PKR and send to a local Pakistani bank account or JazzCash and Easypaisa mobile wallets, from a $1 minimum fee.

- Balance features: Access to 3.2% annual rewards on USD balance paid daily, plus zero-fee investing in 500+ US stocks, ETFs, and gold indices from $1.

The Standard plan costs $0 per month and includes full ACH details and account opening in under 10 minutes using a passport or national ID.

nsave is not a bank. Funds are not FSCS-protected. Customer funds are held in regulated UK and EEA financial institutions, separated from company funds, and protected through safeguarding rules designed for electronic money services.

2. ElevatePay

ElevatePay entered Bangladesh in 2024 as one of the few USD account platforms built specifically for emerging-market freelancers, offering free ACH receiving via an FDIC-insured US partner bank, competitive BDT conversion, and direct bKash transfers. To receive client payments with a free US account and no ACH receiving fee, ElevatePay provides a USD account with a US routing number and account number for Pakistani users.

Pakistani users on r/PakistaniTech discussed ElevatePay alongside Wise directly. One user who used both noted that ElevatePay supports only USD, not EUR or GBP.

3. Payoneer

To receive payouts from Upwork, Fiverr, Amazon, or other integrated marketplaces, Payoneer accepts those transfers but generally applies a 1% receiving fee (or platform-specific flat fee) passed down to the user. Payoneer works well when your income comes from marketplace platforms that already integrate with Payoneer directly.

Pakistani users in r/PakistaniTech confirm that as of 2026, Payoneer connects seamlessly to JazzCash as well as local bank accounts, and that transfers typically arrive in 1 to 4 hours.

One user mentioned: "My company pays me through Payoneer, which is far better than Wise." Where Payoneer may fall short is outside that marketplace ecosystem.

Direct client ACH transfers may also carry a 1% fee. Card-funded payments can cost up to 3.99% plus a country-specific fixed fee (often $0.49).

As of 2026, an annual account fee of $29.95 may apply if you receive less than $6,000 USD in total payments over a 12-month period. Payoneer does not offer rewards on USD balances or investment features. Payoneer may be a good choice when your clients already use Payoneer, or when you receive payouts from Amazon or Fiverr. For direct client payments, alternative fintech platforms like nsave are more cost-effective.

4. Hawala

To receive USD via ACH or hold USDC and USDT alongside USD, Hawala provides a US-based account backed by Lead Bank, with a full routing number and account number accepted by most US payroll systems.

Hawala supports 2 currencies in one account: USD and EUR. It also accepts stablecoin balances including USDC, USDT, PYUSD, and EURC, which makes it a relevant option for remote workers whose employers pay via stablecoin rails.

Hawala is newer than Payoneer and may have a smaller established user base. That is a consideration if platform longevity matters to you.

nsave vs ElevatePay vs Payonner vs Hawala

*Payoneer annual fee of $29.95 applies in some account tiers as of 2026.

For a Pakistani user who needs the most complete USD account covering receiving, holding, rewards, and investing, nsave covers the most ground at $0 per month on the Standard plan.

What Is the Best Wise Alternative in Pakistan for a Freelancer?

For a freelancer earning from Upwork, Fiverr, or direct client contracts, nsave provides one of the strongest overall workflows.

The receiving flow works in 4 steps:

- You share your nsave ACH routing number and account number with the platform or client as your payout destination.

- USD lands in your nsave account directly, with no receiving fee.

- You can hold USD plus earn 3.2% annual rewards on your balance, paid daily.

- You can convert to PKR and send to your local bank account, JazzCash, or Easypaisa when needed, from a $1 minimum fee.

ElevatePay and Hawala are also alternatives if you want a pure receiving account without the added features from nsave. Payoneer also fits freelancers already embedded in its marketplace ecosystem, particularly those on Upwork or Amazon.

What Is the Best Wise Alternative in Pakistan for a Remote Worker?

For a remote worker receiving a regular USD salary via Deel, Gusto, or direct wire transfer, nsave handles the full receiving and holding workflow. ACH details work with domestic US payroll systems and PKR conversion sends to your local account when needed.

Payoneer is often less suited to remote worker payroll, since it is built around marketplace payouts rather than employer-to-employee salary transfers.

It should be known that Wise income received and then transferred to a local bank may carry a different FBR classification than income received via a dedicated ACH account. If accurate freelance income classification matters for your tax position, this is worth discussing with a local tax consultant.

What Is the Best Wise Alternative in Pakistan for E-Commerce Sellers and Dropshippers?

For e-commerce sellers and dropshippers receiving from Amazon, eBay, or Shopify, Payoneer has the direct marketplace integrations. Sellers withdraw Amazon and eBay proceeds directly to their Payoneer account without an additional transfer step.

nsave covers the holding and conversion side of that workflow more cost-effectively. USD sitting in your account between orders can earn 3.2% annual rewards daily, and the investing feature allows surplus working capital to generate returns while not deployed in inventory.

For sellers with multi-currency supplier payments, WorldFirst is also used in this segment, though availability for Pakistani registered businesses should be confirmed directly.

Investments involve risks, including the potential loss of capital. Past performance is not indicative of future results. Data provided is for illustrative purposes only. Consult a licensed financial adviser before making any investment decisions. Investment accounts are provided by a third-party broker dealer.

Can WorldFirst Be Used in Pakistan?

For sellers with multi-currency supplier payments, WorldFirst may be an option for E-Commerce Sellers and Dropshippers . As of 2026, WorldFirst officially supports Pakistani-registered businesses as well as individual freelancers. Their 'World Account' allows Pakistani users to open local receiving accounts in 15+ major currencies, collect funds from over 130 marketplaces (including Upwork and 1688), and pay Chinese or global suppliers directly .

What Is the Best Wise Alternative in Pakistan for Startups and SMEs with International Clients or Suppliers?

For a registered Pakistani business with international clients or suppliers, nsave Business covers multi-currency receiving in USD, EUR, and GBP, bulk payroll via CSV, and local PKR conversion, with no US LLC requirement.

The receiving workflow runs in 3 steps:

- Receive client payments via SWIFT or ACH into your nsave Business account.

- You can hold in USD, EUR, or GBP while awaiting conversion.

- Pay suppliers or convert to PKR for operational costs.

A structural limitation applies to Pakistani businesses using local bank ESFCAs, which are Exporter's Special Foreign Currency Accounts. These accounts accept only SWIFT transfers and do not support ACH receiving. For clients paying via US domestic rails, a platform like nsave is necessary to receive those payments before routing them further.

Whichever platform a business uses for receiving, what happens to USD between receipt and conversion determines the real cost. A USD account that earns on idle balance, invests surplus, and allows you to convert when you desire may deliver more value than one that functions purely as a pass-through.

How to Receive, Hold, and Convert USD with nsave

To receive international payments with nsave, you share your dedicated US routing number and account number with your client, employer, or platform as the payout destination.

The full workflow from receiving to PKR runs in 5 steps:

- You share ACH details with your client, platform, or employer as the payout destination.

- USD lands in your nsave account via ACH from Upwork, Fiverr, Deel, or direct client transfer.

- You can hold USD and earn 3.2% annual rewards paid daily on your USD balance.

- You can convert to PKR and send to your local Pakistani bank account or JazzCash and Easypaisa wallet from a $1 minimum fee.

- You may also invest directly into US stocks, ETFs, or gold indices from $1 with no order fees.

Pakistani freelancers and remote workers have spent years routing income through platforms that were built for other markets and treat Pakistan as an edge case. The infrastructure described in this article exists specifically for users in that position. A USD account that accepts ACH, earns on your balance daily, and converts to PKR at a cost below $1.50 per transfer is available today with a ten-minute sign-up. What you do with that account depends entirely on where your income comes from and how quickly you need it in PKR.

The information in this article is provided for general informational and educational purposes only and does not constitute financial, legal, or tax advice from nsave or any of its affiliates. It is not a substitute for advice from a qualified financial adviser. We make no representations or warranties, whether expressed or implied, that the content is accurate, complete, or up to date.

Fees, exchange rates, incentives, and product availability may change and can vary by user and jurisdiction. Examples are illustrative only. Before making any financial decisions, seek advice from a qualified financial adviser who can assess your individual circumstances and objectives.

nsave helps freelancers and professionals from Bangladesh, Nigeria, Pakistan, Egypt, and other emerging markets receive and manage USD abroad. As a non-bank payment provider, your money is not protected by the Financial Services Compensation Scheme (FSCS). Customer funds are held in regulated, UK and EEA financial institutions, separated from company funds, and protected through safeguarding rules designed for electronic money services.