How to Open a USD Account in Bangladesh

This guide is for Bangladeshis returning from abroad, non-resident Bangladeshis (NRBs) maintaining ties to Bangladesh, anyone working for an international organisation receiving foreign income, and freelancers and remote workers earning in USD from international clients. By the end, you will know which account type fits your situation, what documents each requires, and which banks deliver the strongest USD account experience.

The information provided in this article is for informational and educational purposes only and should not be construed as financial advice. Before making any financial decisions, it is highly recommended that you seek advice from a qualified financial adviser who can consider your individual financial circumstances and objectives.

The Four Types of USD Accounts in Bangladesh

Bangladesh Bank authorises 3 types of foreign currency accounts that individuals can hold at local Authorised Dealer banks , Private FC Accounts, NFCD Accounts, and RFCD Accounts , plus a fourth category: digital USD accounts from international fintech platforms such as nsave and ElevatePay, which operate outside the local banking framework and are the primary option for freelancers receiving ACH payments from platforms like Upwork and Fiverr.

No permission from Bangladesh Bank is required to open a Private FC, NFCD, or RFCD account. Any Authorised Dealer bank branch can open them. Both NFCD and RFCD accounts hold USD, EUR, GBP, JPY, AUD, CAD, CHF, CNH, and SGD , CNH and AUD confirmed as additions under FE Circular No. 10/2024.

Private FC Account

A Private FC Account is a savings-type foreign currency account available to NRBs, foreign nationals, and eligible resident Bangladeshis who receive salary in foreign currency from abroad, with no minimum deposit required to open.

Who can Open a Private FC Account?

A Private FC account is open to the following individuals:

- Bangladeshi nationals working or residing abroad (NRBs)

- Foreign nationals residing abroad or in Bangladesh

- Foreign missions and their expatriate employees

- Foreign firms registered abroad and operating in Bangladesh

- Bangladeshi nationals working in foreign or international organisations in Bangladesh, where salary is paid directly in foreign currency\

What are the Funding sources of Private FC Account?

4 major funding sources of a private FC Account includes:

- Inward remittances through banking channels

- Foreign currency cash,

- Traveller's cheques,

- Transfers from other FC accounts.

What are the Key features of a Private FC Account?

The 4 key features of a private FC account includes:

- No initial deposit required for Bangladeshis going abroad for employment

- The account continues after returning to Bangladesh

- Balance converts to BDT, transfers abroad through banking channels, or withdraws as cash when travelling (up to USD 2,000 per trip)

- Interest applies when the balance holds as a term deposit of at least USD 1,000 for one month or longer

What are the Documents typically required to Open a Private FC Account?

The top 5 documents to open a private FC account includes:

- Passport (first 6 pages and relevant visa page)

- Proof of employment or residence abroad (job certificate, valid visa)

- Completed account opening form

- Nominee information and photograph

- Address verification

NFCD Account

An NFCD (Non-Resident Foreign Currency Deposit) account is a term deposit account for non-resident Bangladeshis, offering interest exempt from income tax , with a minimum deposit of USD 1,000 and terms of 1, 3, 6, or 12 months.

The NFCD is the strongest interest-earning option in Bangladesh's local bank framework. Its tax-free status and benchmarked ceiling rates make it the right tool for NRBs who want to grow USD savings in Bangladesh without paying local income tax on the returns. That said, it is a term deposit, money locks for the chosen term and cannot be withdrawn early without penalty.

Who can Open an NFCD Account?

An NFCD account is open to the following individuals:

- Bangladeshi nationals residing and working abroad

- Bangladeshis with dual citizenship residing abroad

- Bangladeshi nationals serving in Bangladesh missions abroad

- Government and autonomous organisation employees posted abroad

What are the Key Features of an NFCD Account?

The top 6 features of an NFCD Account includes:

- With a term deposit, your funds are locked for your chosen term of 1, 3, 6, or 12 months.

- Any interest earned is fully tax-free in Bangladesh.

- The minimum deposit required is USD 1,000.

- Upon maturity, your balance can be converted to BDT, transferred abroad, or renewed for another term.

- The account is operable from abroad, with documents submitted through a Bangladesh mission or reputable bank.

- Approved currencies include USD, EUR, GBP, JPY, AUD, CAD, CHF, CNH, and SGD, as outlined in FE Circular No. 10/2024.

Interest rate structure (FE Circular No. 10/2024):

What Are the Documents Required to Open an NFCD Account?

The top 4 documents needed to open an NFCD account includes:

- Passport with valid visa or residency documentation

- Employment certificate or proof of overseas posting

- Completed account opening form (submittable from abroad)

- Nominee information

For example: a Bangladeshi nurse working in Saudi Arabia who wants to accumulate USD in Bangladesh whilst earning tax-free interest uses an NFCD 12-month term deposit , the account type is designed precisely for that situation.

RFCD Account

An RFCD (Resident Foreign Currency Deposit) account is for resident Bangladeshis who return from travel abroad , it holds the foreign currency they physically bring back, up to USD 10,000 without a customs declaration, and allows free conversion to BDT or transfer abroad at any time.

The RFCD is the most accessible local bank FC account for resident Bangladeshis. It requires no overseas employment and no inward wire transfer. It simply needs a passport with a return entry stamp and the foreign currency physically carried back from the trip. That constraint , cash only, no wire receiving , also defines its limit: the RFCD is a travel and savings account, not a receiving account for freelance income.

Who Can Open an RFCD Account?

Any Bangladeshi resident aged 18 or above who has returned from travel abroad with foreign currency. This is a residents-only account, not applicable to NRBs.

What are the Deposit rules of an RFCD Account?

The deposit rules of an RFCD account includes:

- Up to USD 10,000 (or equivalent) in cash deposited without any customs declaration

- Amounts above USD 10,000 accepted without an upper cap, provided the traveller obtains a Foreign Money and Jewellery (FMJ) declaration form from customs on arrival (in force since February 2020)

What are the Key features of an RFCD Account?

The 6 key features of an RFCD Account includes:

- NFCD savings accounts have no lock-in period, giving you full flexibility over your funds.

- Your balance can be converted to BDT at any time.

- Funds can be transferred abroad for legitimate purposes, including international education, medical expenses, and travel.

- Account holders can issue up to two supplementary international cards to dependents, giving family members direct access to the foreign currency balance for tuition and living expenses abroad, confirmed as of March 2026.

- When travelling abroad, you can withdraw up to USD 2,000 in cash directly from your balance.

- Most banks do not require a minimum balance to maintain the account.

What Are the Documents Required to Open an RFD Account?

As of March 2026, the 4 mandatory documents required to open an RFCD account includes:

- Passport with entry stamp (proof of return from abroad)

- Address verification (utility bill)

- Proof of income and occupation

- Completed account opening form

Digital USD Accounts (nsave / ElevatePay)

Digital USD accounts from international fintech platforms , such as nsave and ElevatePay , are non-resident USD accounts that give Bangladeshi freelancers and remote workers personal ACH routing and account numbers for receiving payments directly from Upwork, Fiverr, Deel, Toptal, and international clients. They operate outside Bangladesh's local bank framework and are the only account type on this list that accepts ACH transfers.

This is the account type the freelancer gap points directly to. Local bank FCY accounts, Private FC,NFCD,RFCD accept SWIFT only for inward transfers, and the RFCD accepts no wire transfers at all.

ACH is the US domestic bank transfer system that Upwork, Fiverr, Deel, and most US-based platforms use to pay workers. None of Bangladesh's local bank FC accounts can receive ACH. Digital fintech accounts can , and that single difference is what makes them the primary USD receiving tool for platform-based freelancers in Bangladesh.

*nsave is not a bank. Funds are not FSCS-protected. nsave is a non-resident USD account for individuals, not a substitute for a full-service Bangladeshi bank account for savings, loans, or government services.

nsave

nsave is a global USD payment platform that gives Bangladeshi, Nigerian, Pakistani, and other emerging market freelancers a free personal USD account with ACH routing and account numbers, free SWIFT wire receiving, 3.2% annual rewards on idle USD paid daily, a virtual Debit Card, and BDT withdrawal, including direct bKash in seconds.

ElevatePay

ElevatePay is a US-based fintech that gives Bangladeshi freelancers a free USD account held with Bangor Savings Bank (FDIC member, deposit protection up to $250,000) with free ACH receiving, instant bKash transfers, and competitive BDT conversion

A digital USD account is one of the easiest ways to get paid from Upwork, Fiverr, Deel, Toptal, PeoplePerHour, or direct international clients via ACH, hold your earnings in USD, earn on them daily, convert to BDT on demand, and withdraw straight to bKash without a branch visit.

Investments involve risks, including the potential loss of capital. Past performance is not indicative of future results. Data provided is for illustrative purposes only. Consult a licensed financial adviser before making any investment decisions. Investment accounts are provided by a third-party broker dealer.

Who Can Open a USD Account in Bangladesh?

Eligibility for a foreign currency account in Bangladesh depends on which account type matches your situation , NRBs and overseas Bangladeshis use Private FC or NFCD accounts, resident Bangladeshis returning from travel use RFCD accounts, and freelancers receiving ACH platform payouts use digital fintech accounts.

Traditional RFCD and Private FC accounts are restricted to physical cash and specific foreign employment, which left most freelancers without a formal way to receive international payments. Bangladesh Bank addressed this in February 2023 by mandating that individual freelancers are entitled to open Exporter's Retention Quota (ERQ) accounts, allowing them to receive inward remittances directly from platforms like Upwork and Fiverr, as well as from direct foreign clients.

Under this facility, freelancers in the ICT and software sectors can retain between 35% and 70% of their foreign earnings in USD (subject to current central bank caps) to cover legitimate business expenses such as software licenses, hosting, and international advertising. Most local banks offer ERQ accounts as a bundle that includes a BDT savings account and an international debit card linked to the USD balance.

Documents You'll Need to Open an Account

To open a foreign currency account at a Bangladeshi bank, you need your passport, proof of overseas status or residency, address verification, proof of income, and nominee information; the exact list varies by account type.

Some banks, including Trust Bank and EBL, require an introduction from an existing customer of at least six months' standing; you should confirm this with your chosen bank before visiting.

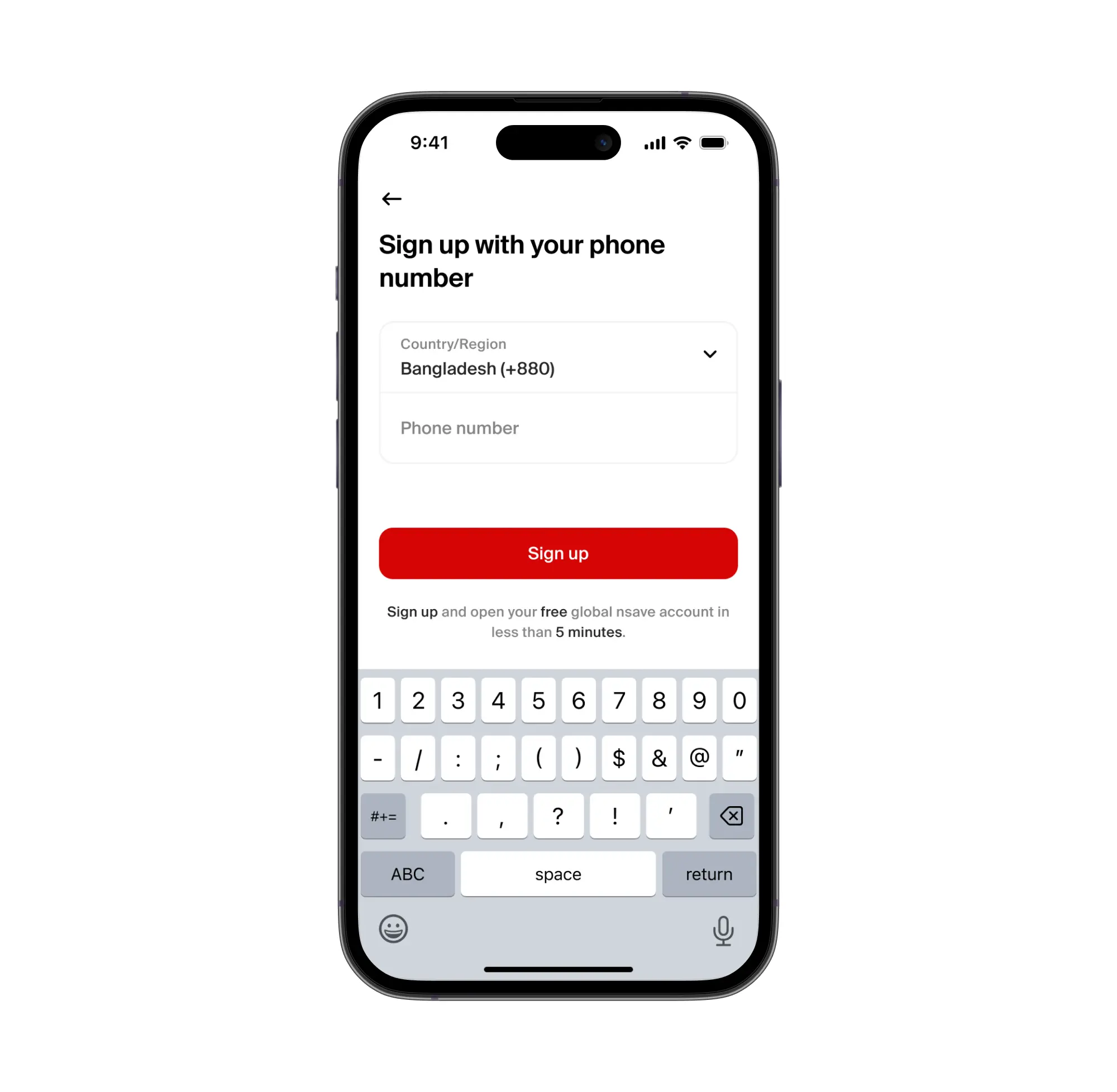

For digital accounts such as nsave and ElevatePay, identity verification is done entirely through the app using your Bangladeshi passport or NID, with no branch visit, no paper forms, and verification completing in under 10 minutes.

Which Banks Offer Foreign Currency Accounts?

All Authorised Dealer bank branches in Bangladesh open foreign currency accounts. The 5 banks most frequently used for FCY account services are Standard Chartered, Eastern Bank (EBL), City Bank, Dutch-Bangla Bank (DBBL), and BRAC Bank.

Standard Chartered Bangladesh

Standard Chartered Bangladesh offers RFCD accounts with no minimum balance requirement, backed by strong international banking infrastructure and online account access. The account is well-suited to professionals and high-net-worth individuals who prioritise a globally recognised banking name.

Eastern Bank (EBL)

Eastern Bank (EBL) has a strong focus on non-resident Bangladeshis through its EBL Global account, which comes with a linked Global Visa debit card for international use and 24/7 internet banking. Its dedicated Freelancer Suite account makes it one of the most consistently recommended options for freelancers receiving international income.

City Bank

City Bank is well regarded for its digital banking experience and foreign currency account management. It also made headlines as the bank that launched Google Pay in Bangladesh in June 2025, reflecting its active push into fintech integration.

Dutch-Bangla Bank (DBBL)

Dutch-Bangla Bank (DBBL) operates Bangladesh's largest ATM and electronic banking network, making it a practical choice for users who want wide cash access alongside foreign currency account functionality.

BRAC Bank

BRAC Bank has a strong focus on SME and non-resident Bangladeshis, making it well-suited to business owners and professionals with international income connections.

That said, all Authorised Dealer (AD) banks in Bangladesh are permitted to open these accounts, so your final choice will likely come down to your existing banking relationship, the quality of their digital banking experience, and how convenient their branch is for your initial document submission.

Limitations of Local Bank USD Accounts for Freelancers

Local bank foreign currency accounts in Bangladesh carry 4 structural limitations that prevent them from working as receiving accounts for freelancers and remote workers on international platforms.

1. Cannot receive ACH transfers from foreign clients: ACH is the US domestic bank transfer system that Upwork, Fiverr, Deel, and most US-based payment platforms use to pay workers. Local Bangladeshi bank accounts , including all FCY account types , cannot receive ACH transfers. They accept SWIFT only. Most freelance platform payouts travel via ACH, not SWIFT.

2. RFCD is funded by physical cash only. The RFCD account , the most accessible option for resident Bangladeshis , cannot receive wire transfers of any kind. It holds only foreign currency physically carried back into Bangladesh from travel. It is a savings account, not an income-receiving account.

3. Branch visit required to open: Opening an FCY account at a Bangladeshi bank requires visiting a branch with original documents. App-based opening is not available for any local FCY account type.

4. SWIFT receiving carries sender-side costs: Private FC accounts accept SWIFT inward wire transfers , but SWIFT transfers typically cost USD 15–50 at the sending bank. Most freelance platforms do not offer SWIFT as a payout method, and clients making manual SWIFT transfers absorb that cost or pass it on.

These 4 limitations converge on one conclusion: for freelancers receiving ACH platform payouts, local bank FCY accounts are the wrong tool. The right tool is a digital fintech account with personal ACH routing details , which is exactly what nsave and ElevatePay provide.

How to Receive USD Earnings and Convert to BDT with nsave

To receive USD from international clients or platforms and convert to BDT at a time of your choosing, open a nsave USD account, share your ACH routing number and account number as your payout destination, and initiate a BDT withdrawal when you are ready.

Step 1: Open Your nsave USD Account

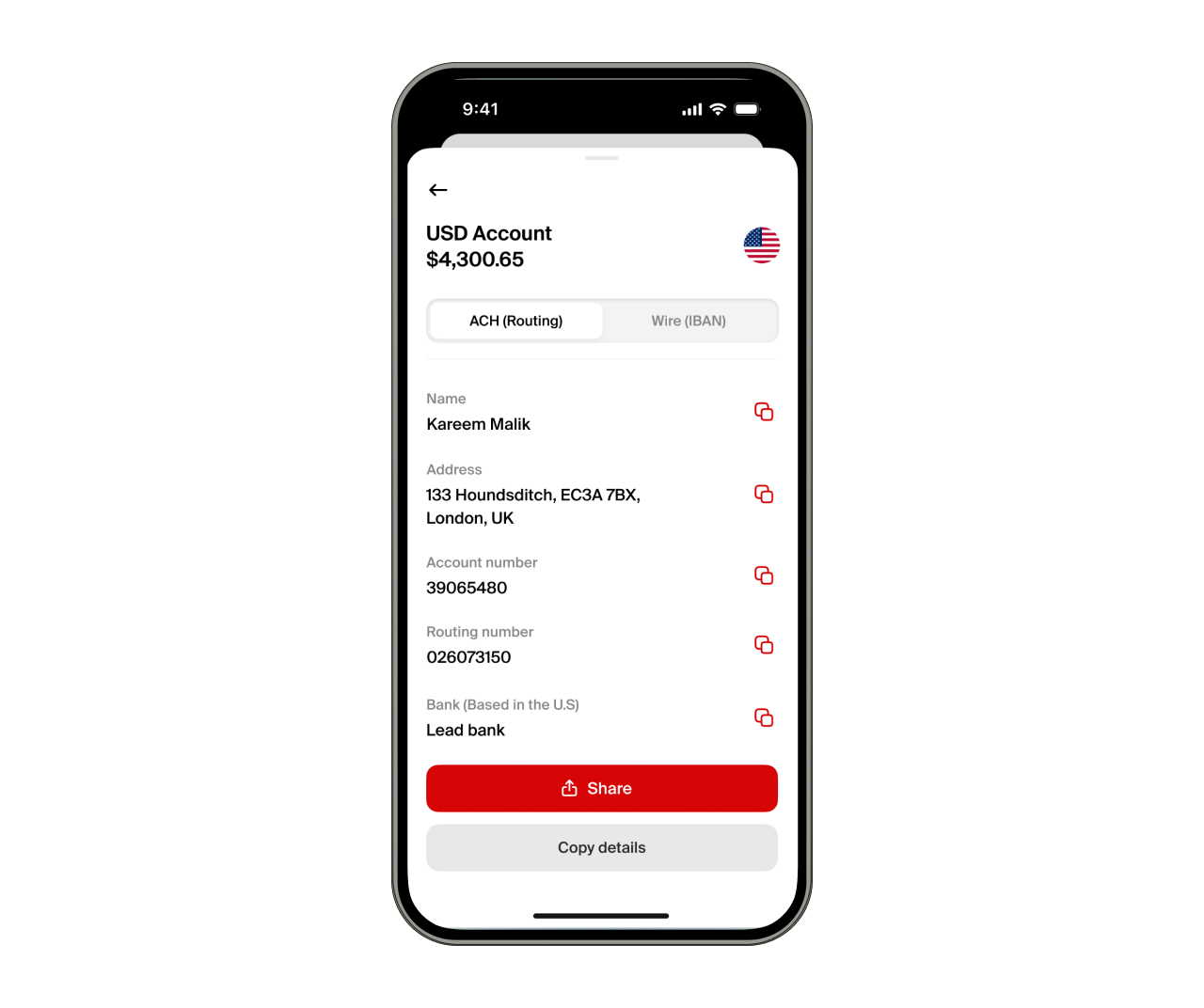

To open your nsave USD account, download the nsave app and verify your identity using your Bangladeshi passport or NID. The Standard plan carries no monthly fee. Verification completes in under 10 minutes with no branch visit required. Once verified, your account dashboard displays your personal ACH routing number and account number , real US account details, assigned to you individually, accepted by any international client or platform that pays via US transfer.

Step 2: Share Your nsave ACH Details as Your Payout Destination

To receive USD via nsave, update your payout settings on your platform:

- Upwork: Settings → Get Paid → US Bank (ACH) → enter your nsave routing number and account number

- Fiverr: Earnings → Withdraw → Bank Transfer → same details

- Toptal, Freelancer.com, PeoplePerHour: follow each platform's bank payout setup; enter the same ACH details

- Direct clients: add your nsave ACH routing and account number to your standard invoice

- SWIFT-paying clients (UK, EU, Australia): share your nsave SWIFT receiving details from the app

Step 3: Earn USD While Holding

nsave provides you the opportunity to earn 3.2% annual rewards on your USD balance on the Standard plan, paid daily, or 4.2% on the Pro plan at $9.99 per month. You can hold your USD for weeks or months, if you desire. nsave also gives you access to invest in US stocks, ETFs, gold indices, or bonds from as little as $1 with no order fees, with Sharia-compliant options available.

Investments involve risks, including the potential loss of capital. Past performance is not indicative of future results. Data provided is for illustrative purposes only. Consult a licensed financial adviser before making any investment decisions. Investment accounts are provided by a third-party broker dealer.

Step 4: Convert to BDT and Withdraw

To withdraw from nsave, tap Withdraw in the app and send funds to either bKash or any local Bangladeshi bank account, with the exact BDT amount shown before you confirm.

Frequently Asked Questions

1. Can I keep my USD in Bangladesh without converting to BDT?

Yes, Bangladeshi freelancers retain USD without converting to BDT through 2 channels: an ERQ (Exporter's Retention Quota) account at a Bangladesh Bank-authorized institution such as City Bank or Standard Chartered, or a USD-holding fintech account such as nsave, ElevatePay, or Payoneer that holds balances in USD until the account holder initiates a BDT withdrawal.

2. Does Bangladesh Bank allow freelancers to hold foreign currency?

Yes, Bangladesh Bank permits IT and service exporters to retain up to 60%–70% of repatriated earnings in an ERQ account under 2026 guidelines. The remaining portion converts to BDT at the point of entry into the Bangladeshi banking system.

3. What happens to my USD if I don't withdraw within 30 days?

No automatic conversion applies to balances already held in an ERQ or fintech account but incoming export proceeds arriving at a local bank trigger a 30-day decision window. Within 30 days, the account holder allocates the ERQ-eligible portion to retain as USD; the remainder the bank converts to BDT. This 30-day rule does not apply to funds held in international fintech accounts such as nsave, as those funds have not yet entered the Bangladeshi banking system.

4. Can I use a USD account in Bangladesh to pay for subscriptions like Netflix or Adobe?

Partially, local ERQ accounts do not natively support recurring international subscription payments unless the bank issues a Dual Currency Card or International Debit Card linked to the ERQ account. Freelancers pay for subscriptions such as Netflix, Adobe, Youtube Premium, and Canva using USD virtual cards from Payoneer, nsave, or PriyoPay, which carry fewer restrictions than local bank-issued cards on international billing systems.

5. Do USD accounts in Bangladesh qualify for the 2.5% government remittance incentive?

Yes, with conditions, the 2.5% incentive applies to the portion of foreign currency converted to BDT through official channels. USD retained in an ERQ account does not trigger the incentive until liquidated into local currency. Transfers exceeding $5,000 require supporting documentation such as a Freelancer ID or proof of work to qualify.

6. Can I receive a salary in USD from a foreign employer in Bangladesh?

Yes, Bangladeshi residents receive USD salaries from foreign employers through 2 methods: a direct SWIFT transfer into an ERQ or foreign currency account at a Bangladesh Bank-authorized institution, or an ACH or wire transfer into a fintech account such as Payoneer, ElevatePay, or nsave, which then routes funds into Bangladesh.

7. Will my USD account in Bangladesh affect my tax return?

Yes, under the Income Tax Act 2023, all foreign income must be declared in the annual tax return regardless of whether the balance remains in USD or converts to BDT. Foreign currency income is treated as accrued income at the point of earning. Freelancers retain bank certificates and Encashment Certificates as documentation confirming the source and entry of funds.

8. Can I send USD from my Bangladesh account to someone abroad?

Limited, outward transfers from ERQ accounts are permitted for bonafide business purposes such as software licenses, hosting, and digital marketing up to $10,000 per year. Personal transfers to friends or family abroad from a local ERQ account require specific Bangladesh Bank approval. Fintech accounts such as nsave and ElevatePay offer greater outward transfer flexibility as they operate under international jurisdictions outside Bangladesh Bank's direct outward remittance rules.

9. Is there a limit on how much USD I can hold in Bangladesh?

Yes, the holding limit ties directly to the ERQ retention quota. A freelancer earning $1,000 with a 70% quota retains $700 as USD; the remaining $300 converts to BDT. No maximum balance cap applies provided every retained dollar falls within the account holder's legal retention percentage.

10. Can I open a USD account in Bangladesh as a student?

Yes, with proof of income student status does not disqualify an applicant from an ERQ account, but income documentation does. Students without freelance earnings, a scholarship record, or equivalent foreign income proof cannot open an ERQ account at a Bangladesh Bank-authorized institution. Students without qualifying documentation use fintech apps or Student Files for education expenses to manage foreign currency instead.

11. Can I Use Payoneer to Receive and Hold USD in Bangladesh?

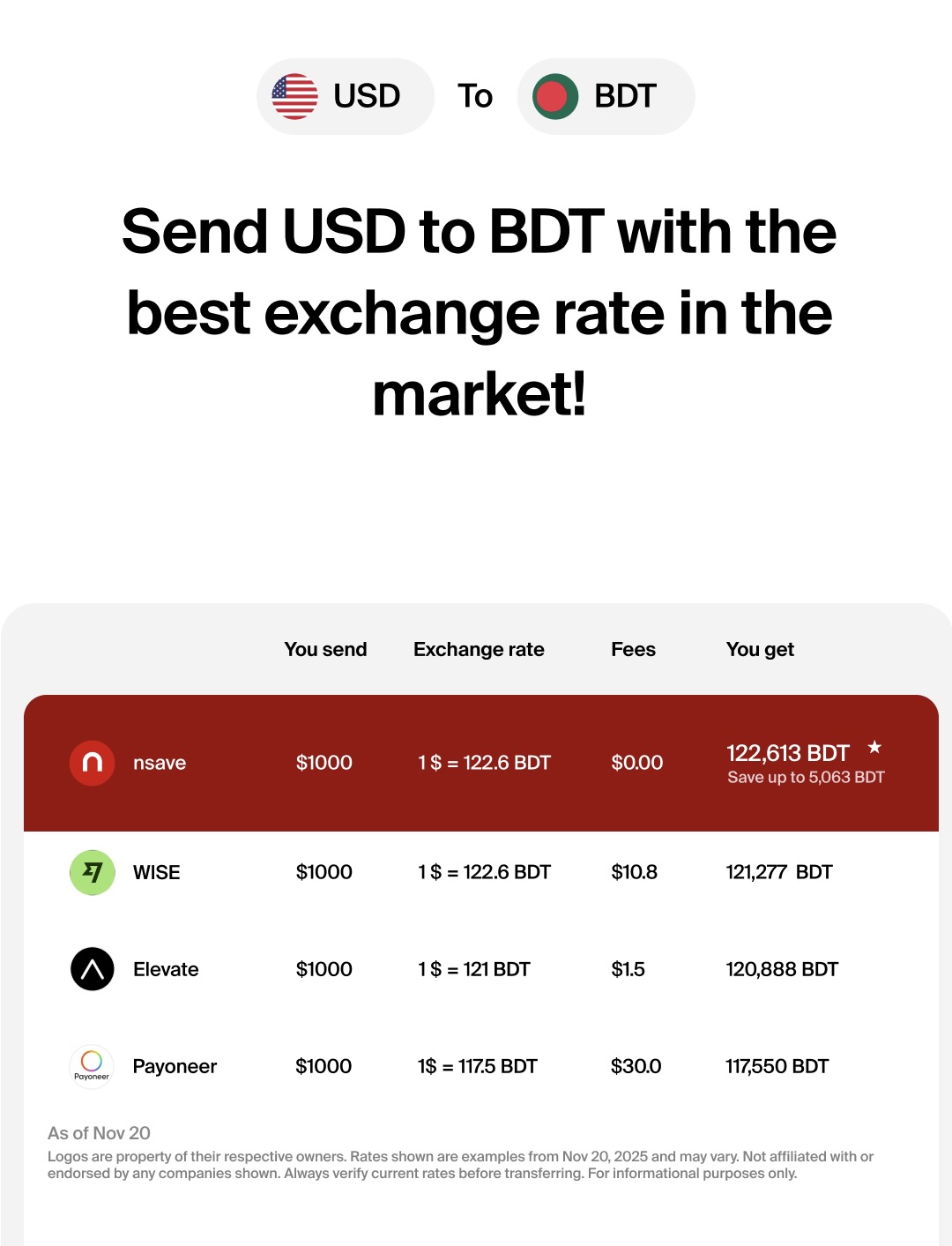

Payoneer is widely used by Bangladeshi freelancers on Upwork and Fiverr, and supports BDT withdrawals to local bank accounts and direct bKash transfers at BDT 7 per BDT 1,000. Payoneer accepts ACH and SWIFT, integrates natively with over 2,000 platforms, and has operated in Bangladesh longer than any other option on this list.

12. Can I Use Wise to Hold and Convert USD in Bangladesh?

As of March 2026, Wise has restricted functionality in Bangladesh. According to Wise, while you can send Bangladeshi Taka (BDT) to bank accounts, bKash, or Nagad, residents cannot open a Wise multi-currency account, order a Wise card, or get USD account details to receive payments directly.

Key Takeaways

Bangladesh Bank authorises 3 types of individual foreign currency accounts at local banks: Private FC Accounts (for NRBs and eligible residents receiving a foreign salary), NFCD Accounts (term deposits for NRBs, with benchmarked tax-free interest), and RFCD Accounts (for resident Bangladeshis returning from travel, funded only with physically carried cash). A fourth category , digital fintech accounts from platforms such as nsave, operates outside the local bank framework and is the primary USD receiving option for freelancers and remote workers on international platforms.

No Bangladesh Bank permission is required to open a Private FC, NFCD, or RFCD account. Any Authorised Dealer bank opens them. Approved currencies for NFCD and RFCD accounts include USD, EUR, GBP, JPY, AUD, CAD, CHF, CNH, and SGD (FE Circular No. 10/2024). Standard Chartered, EBL, City Bank, DBBL, and BRAC Bank are the most commonly used.

For freelancers and remote workers receiving USD from international clients, local bank FCY accounts do not accept ACH platform payouts , they accept SWIFT only. Digital fintech accounts from nsave provide personal ACH routing and account numbers accepted by Upwork, Fiverr, Deel, and other platforms. USD held in nsave earns 3.2–4.2% annually in daily rewards (confirm rates as rates may change), converts to BDT on demand, withdraws directly to bKash in seconds, and requires no branch visit , making it the practical USD receiving solution that complements, rather than replaces, a locally held bank account.

Investments involve risks, including the potential loss of capital. Past performance is not indicative of future results. Data provided is for illustrative purposes only. Consult a licensed financial advisor before making any investment decisions. Investment accounts are provided by a third-party broker dealer

The information in this article is provided for general informational and educational purposes only and does not constitute financial, legal, or tax advice from nsave or any of its affiliates. It is not a substitute for advice from a qualified financial advisor. We make no representations or warranties, whether expressed or implied, that the content is accurate, complete, or up to date.

Fees, exchange rates, incentives, and product availability may change and can vary by user and jurisdiction. Examples are illustrative only. Before making any financial decisions, seek advice from a qualified financial advisor who can assess your individual circumstances and objectives.

nsave helps freelancers and professionals from Bangladesh, Nigeria, Pakistan, Egypt, and beyond receive and manage USD abroad. As a non-bank payment provider, your money is not protected by the Financial Services Compensation Scheme (FSCS).