RFCD Account in Bangladesh

You came back from a business trip to Dubai or a conference in Singapore with USD 5,000 in your pocket. The bank teller wants to convert it to Taka on the spot. You want to hold it in dollars. The RFCD account, Resident Foreign Currency Deposit , is Bangladesh Bank's regulated structure for exactly this situation.

This article is for Bangladeshi residents who travel abroad and return with foreign currency , whether for business, work, or personal reasons. It covers what the account does, who qualifies, what you can deposit, what you can do with the balance, and how to open one.

One policy update worth noting upfront: under FE Circular No. 28, issued 31 October 2024, Bangladesh Bank fully deregulated RFCD interest rates. Each Authorised Dealer bank now sets its own rate.

What is an RFCD Account?

An RFCD account (Resident Foreign Currency Deposit), is a foreign currency account that Bangladeshi residents can open at any Authorised Dealer bank to hold foreign exchange physically brought back from travel abroad, as regulated under GFET Chapter 13, Section III.

The RFCD account lets you hold USD, EUR, GBP, JPY, AUD, CAD, CHF, CNH, or SGD inside Bangladesh without converting to Taka. The balance earns interest and It sits in a foreign currency account, denominated in the currency you deposited.

This account is not for receiving remittances or freelance income from abroad. Earnings sent to Bangladesh via SWIFT, ACH, or any international wire do not qualify as RFCD deposit sources. That distinction matters. If your income arrives digitally from foreign clients or platforms, you need a different account structure entirely.

Who Can Open an RFCD Account?

To open an RFCD account, you must be a Bangladeshi resident aged 18 or above who has physically travelled abroad and brought back foreign currency.

Three eligibility conditions to open an RFCD account include:

- You are ordinarily resident in Bangladesh , not a non-resident, not a foreign national

- You are aged 18 or above

- The foreign currency was physically brought into Bangladesh from abroad

A common misconception is that freelancers receiving payments from Upwork, Fiverr, or Deel via wire transfer cannot deposit those earnings into an RFCD account. The permitted deposit source is physical foreign exchange carried in personally from travel. The digital income question requires a separate solution, covered further below.

A mandatory document for opening an RFCD account is a copy of your passport with the arrival seal (stamp) from your most recent trip. The bank needs to verify that you have actually returned from abroad to establish your eligibility "at the time of return." Without the arrival stamp, the bank cannot process the account opening application.

RFCD vs NFCD Account

The key difference between an RFCD and an NFCD account is residency status: RFCD is for Bangladeshis ordinarily resident inside Bangladesh, while NFCD , Non-Resident Foreign Currency Deposit , is for Bangladeshis living or working abroad.

If you live in Bangladesh and travel abroad for work or business, RFCD is the recommended account type. If you live abroad or are a Bangladeshi national earning income overseas with no permanent address in Bangladesh, NFCD is the recommended account type

What Can You Deposit into an RFCD Account?

To deposit into an RFCD account, the foreign currency must have been physically brought into Bangladesh at the time of your return from travel abroad , accepted in cash notes, traveller's cheques, or drafts.

Six major deposit rules of an RFCD Account apply:

- Cash notes, traveller's cheques, and drafts from personal travel abroad are permitted.

- Up to USD 10,000 or equivalent per trip can be deposited without any customs declaration.

- Any amount above USD 10,000 requires a Foreign Money and Jewellery (FMJ) declaration form, obtained from customs at the port of entry on arrival; there is no upper cap on the declared amount.

- Balances from a separate Foreign Currency (FCY) account cannot be transferred to RFCD.

- Inward remittances and wire transfers from abroad are not permitted.

- Proceeds from export of goods or services, or commissions from business transactions conducted in Bangladesh, cannot be credited.

Since February 2020, Bangladeshis returning from abroad can deposit up to USD 10,000 in cash into an RFCD account without any declaration and amounts above this threshold can still be credited if accompanied by a Foreign Money and Jewellery declaration with no upper cap on the declared amount.

For example, if you return from a business trip to Dubai with USD 8,000 in cash, you can deposit the full amount into your RFCD account at any Authorised Dealer bank without filing any customs form. While the currency must be brought in at the time of your return, you don't necessarily have to deposit it the same day you land. However, banks usually expect you to open/fund the account within a reasonable timeframe (often within 30 days of arrival) to ensure the funds are clearly linked to that specific trip's arrival stamp.

What Can You Do with the Money in an RFCD Account?

Funds held in an RFCD account can be converted to Taka for local spending, sent abroad via bank transfer for legitimate purposes, or used to fund an international debit or credit card.

Five permitted use of an RFCD Account includers:

- Convert to Bangladeshi Taka at the prevailing exchange rate for any local transaction , the balance is freely encashable in BDT at any time

- Send abroad via the banking channel for lawful purposes, including children's tuition fees at foreign universities, medical treatment costs at foreign hospitals, and personal travel expenses

- Endorse foreign currency in your passport for travel, up to USD 2,000 in cash notes per trip and remainder in traveller's cheques or other instruments

- Issue an international debit or credit card against the balance, with up to 2 supplementary cards for dependants

The total amount you can use/endorse is limited only by your available balance in the RFCD account. It does not count towards your annual $12,000 private travel quota

Any resident Bangladeshi returning from abroad can deposit up to USD 10,000 (or equivalent) in cash into an RFCD account without any customs declaration. For amounts exceeding this threshold, there is no upper limit on what can be deposited, provided the traveller obtains a Foreign Money and Jewellery (FMJ) form from customs upon arrival.

These account balances are highly flexible, they can be freely converted to BDT at any time and used for unlimited outward remittances for specific legitimate purposes such as international education, medical expenses, and travel. Furthermore, account holders can now officially use their RFCD funds to support dependants by issuing supplementary dual-currency cards or making direct payments for their tuition and living expenses abroad.

Two actions are not permitted though which are, transferring to a third party's account and using the balance for business transactions sourced from Bangladesh.

Interest on RFCD Accounts

As of March 2026, RFCD accounts earn interest at a rate each Authorised Dealer bank sets independently.

According to Bangladesh Bank's FE Circular No. 28, Bangladesh Bank fully deregulated RFCD interest rates, now each AD bank now determines the rate on a banker-customer basis , no floor and no ceiling apply. The previous benchmark + 1.50% structure, set by FE Circular Letter No. 19 in December 2023, no longer applies.

For balances placed as a term deposit, interest is paid at the term rate for the agreed period , options include 1, 3, 6, or 12 months. If a term deposit is broken before the agreed maturity date, the bank returns the principal but forfeits the accrued interest. Contact your specific Authorised Dealer bank directly for the current rate in your preferred currency.

Taxes on RFCD Accounts

For a RFCD account, Banks are required to deduct withholding tax (TDS) on the interest earned. The rate is typically 10% if you submit a Proof of Submission of Return (PSR) for your income tax, or 15% if you do not.

How to Open an RFCD Account

To open an RFCD account, visit any Authorised Dealer bank branch in Bangladesh with your passport showing the arrival stamp from your most recent trip abroad, fill in the account opening form, and submit the required documents.

Step 1: Choose an Authorised Dealer Bank

Any commercial bank in Bangladesh with Authorised Dealer status can open an RFCD account. Major options include City Bank, BRAC Bank, Eastern Bank Limited (EBL), Standard Chartered Bangladesh, UCB, Mutual Trust Bank, Prime Bank, Agrani Bank, Jamuna Bank, and Premier Bank. Before choosing, compare the term deposit interest rates and the terms for international card issuance across at least 2 or 3 banks, as rates vary and are not published centrally.

Step 2: Gather Your Documents

Submit the following 7 documents to the bank:

- Valid Bangladeshi passport with immigration arrival stamp for the trip against which the deposit is being made

- National Identity Card (NID) or Smart NID

- Completed account opening form from the bank

- FMJ customs declaration form, if the deposit amount exceeds USD 10,000

- Written declaration from the depositor stating the date of return and the amount of foreign currency brought in

- Proof of submission of income tax return (PSR) if the deposit equals or exceeds BDT 1,000,000 , some banks require this

- Nominee photo ID (NID, birth certificate, or passport)

Step 3: Submit the Application and Make Your Deposit

Visit the branch, submit the documents, and bring the foreign currency notes or traveller's cheques physically. The bank verifies the passport arrival stamp against the trip date. Once verified, the account opens and the deposit is credited in the relevant foreign currency , USD, GBP, EUR, or another eligible currency. You generally cannot open an RFCD account with a zero balance.

Most banks require a specific minimum initial deposit to open the account. This amount varies by bank (e.g., USD 1,000 at Standard Chartered, USD 250 at Prime Bank, or similar equivalents in GBP/EUR).

The RFCD account is not opened "empty" to be funded later. The act of depositing the cash you brought back is what opens the account. If you return with only $50, most banks will not open an RFCD account for you because it falls below their minimum opening threshold

Step 4: Activate Your International Card (Optional)

As of March 2026, RFCD account holders can issue up to 2 supplementary international cards to their dependants, giving family members direct access to the foreign currency balance.

Once the account opens, request an international debit or credit card linked to the RFCD balance. This allows the account holder and up to 2 dependants to spend directly from the foreign currency balance abroad or online.

What are the Key Limitations of an RFCD Account

The main limitation of an RFCD account is that it accepts only physical foreign currency brought back from travel abroad , inward remittances, wire transfers, ACH payments, and online payment platforms are not permitted deposit sources.

Four practical limitations of an RFCD Account include:

- Source restriction: Only physical foreign exchange from personal travel abroad qualifies. Upwork earnings, Fiverr payments, SWIFT transfers from foreign employers, and ACH transfers from international clients cannot be deposited

- Per-trip deposit cap without declaration: USD 10,000 per trip can be deposited without Form FMJ; amounts above this require a customs declaration obtained at the port of entry on arrival

- No incoming remittances: Money sent to Bangladesh from abroad via any banking channel cannot land in an RFCD account

- Interest forfeiture on early withdrawal: Breaking a term deposit before maturity forfeits all accrued interest; only the principal is returned

The source restriction is the most important limit for anyone who earns money from abroad digitally. An RFCD account holds foreign currency you physically carry home. If your income arrives digitally from a foreign client, platform, or employer, it needs a different receiving structure. That question , how to hold and use USD earned remotely as a Bangladeshi resident , is what the next section covers.

How to Receive Foreign Income in USD as a Bangladeshi Resident

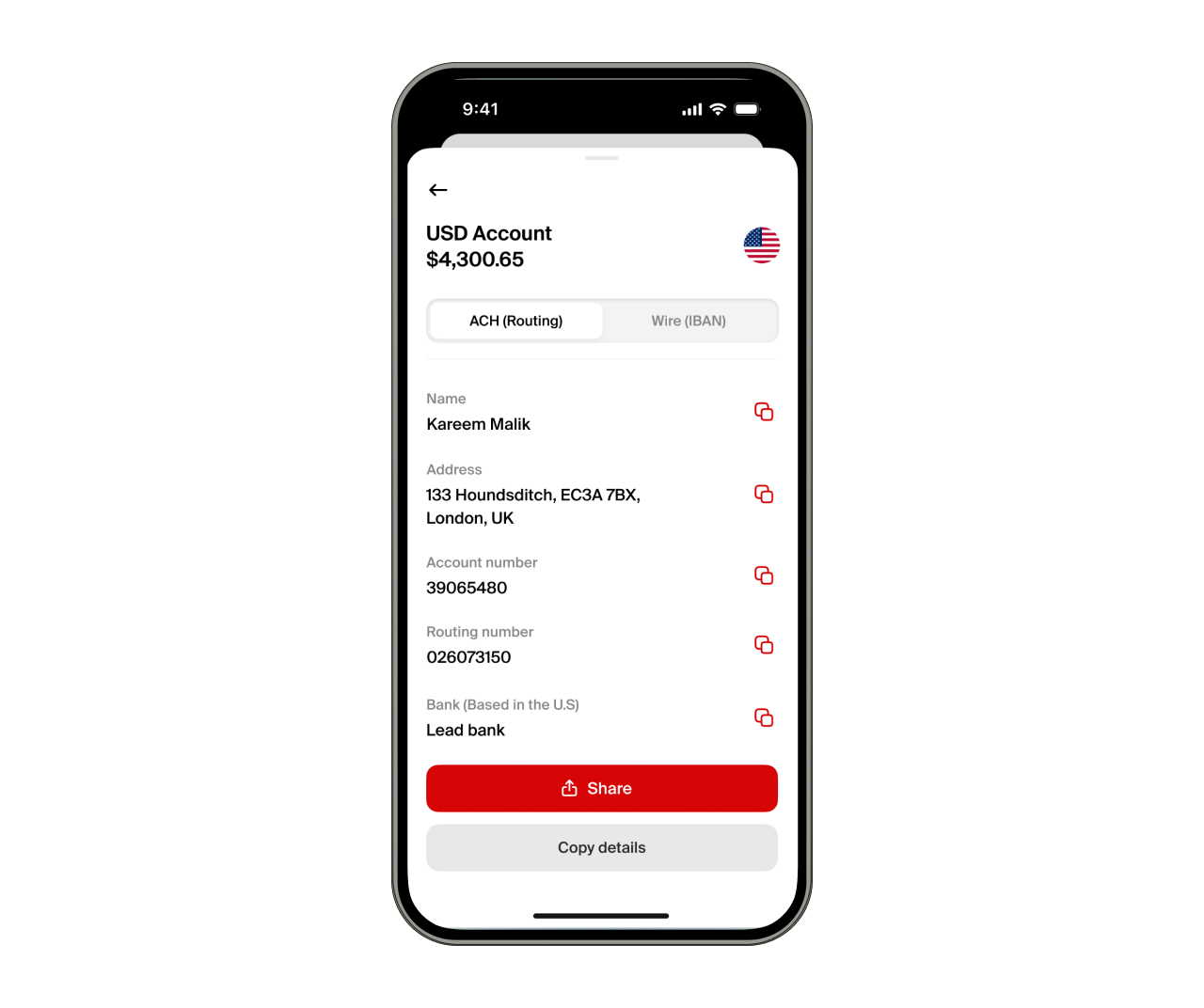

To receive USD income from foreign clients or platforms as a Bangladeshi resident, open a non-resident USD account with nsave , a cross-border payment platform that gives you a personal ACH routing number and account number you can share directly with clients or platforms such as Upwork, Fiverr, and Deel.

If your income arrives digitally , from Upwork, a foreign employer, or an international client , an RFCD account is not the right structure. You need a USD account that accepts international wire transfers and ACH payments. The steps below cover how to set one up, how to hold your earnings in USD while you decide when to convert, and how to move money to your Bangladeshi bank account or bKash when you're ready.

Step 1: Open Your nsave USD Account

To open a USD account with nsave, download the nsave mobile app and complete verification using your passport or national ID. The account opens in under 10 minutes with no branch visit required and no monthly fee on the Standard plan. Once verified, you receive a personal ACH routing number and account number. These are the details you share with any client, freelance platform, or employer that pays via US bank transfer.

New to nsave? Watch how to set up your account in under 10 minutes:

Step 2: Set nsave as Your Payout Destination

To set nsave as your payout destination, share your nsave ACH details with Upwork, Fiverr, Toptal, Deel, PeoplePerHour, or Freelancer.com as the withdrawal account. Payments sent via ACH or SWIFT arrive in your nsave USD account. Receiving via ACH or SWIFT is free on both the Standard and Pro plans.

Step 3: Convert and Send to Your Bangladeshi Account or bKash

To send your USD balance to your Bangladeshi account or bKash, initiate a local currency withdrawal in the nsave app. The app displays the exact BDT amount before you confirm. The minimum payout fee is $1(fees subject to change, check the nsave app for current rates). Funds arrive in your Bangladeshi bank account or bKash directly.

Can I Receive Foreign Earnings via Payoneer in Bangladesh?

To receive foreign earnings via Payoneer in Bangladesh, connect your Payoneer account to Upwork, Fiverr, or your direct client, then withdraw to a local bank account in BDT. Payoneer allows Bangladeshi freelancers to receive payments in USD.

Can I Use Stripe to Accept Client Payments in Bangladesh?

No, stripe is not available in Bangladesh, acccording to Stripe's global availability directory, Stripe does not include Bangladesh on its list of supported countries as of March 2026, and no official entry timeline exists.

This blocks not just direct Stripe usage but also downstream platforms that rely on Stripe as their payment infrastructure, including Ko-fi and Lemon Squeezy. Bangladeshi freelancers and digital product sellers who need to accept USD from international clients cannot use these tools natively.

As of 2026, there is no Stripe equivalent in Bangladesh, meaning most users default to Payoneer for the international payment gap, even though Payoneer does not offer the same direct API and merchant capabilities as Stripe.

The practical alternative for receiving client payments in USD is an nsave USD account with ACH details , suitable for invoicing clients directly and receiving platform payouts from Upwork, Fiverr, and Deel.

Can I Use Mercury to Receive Business Income in Bangladesh?

According to Mercury Bank's official support guidelines, Mercury Bank officially stopped supporting business accounts for founders and companies with physical or residential addresses in Bangladesh. The decision follows previous restrictions Mercury placed on other regions (such as Pakistan in 2024). The nsave business account supports USD, EUR, and GBP, with payroll, supplier payments, and expense management.

Key Takeaways

An RFCD account is a foreign currency deposit account for Bangladeshi residents who physically bring back foreign exchange from travel abroad. Open one at any Authorised Dealer bank in Bangladesh using your passport, NID, and proof of travel.

The single eligibility condition that matters most: the source of funds must be physical travel. Earnings sent digitally from a foreign client, platform, or employer cannot be deposited.

For Bangladeshi residents who earn income remotely from foreign clients , via Upwork, Fiverr, Deel, or direct wire , the right structure is a USD account that accepts inward transfers.

FAQs About RFCD Accounts

Can a freelancer use an RFCD account to receive Upwork or Fiverr payments?

To receive Upwork or Fiverr payments in Bangladesh, use a platform that accepts inward wire transfers , an RFCD account does not qualify. RFCD accounts cannot receive inward remittances or wire transfers. Earnings from Upwork, Fiverr, or any foreign platform sent to Bangladesh via SWIFT or ACH are not a permitted deposit source.

Is RFCD interest taxable?

Yes, interest earned on an RFCD account is taxable. Unlike Non-Resident Foreign Currency Deposit (NFCD) accounts or Wage Earners' Development Bonds, the interest income from a Resident Foreign Currency Deposit (RFCD) account does not enjoy tax-exempt status.

How long after returning from abroad can I deposit?

Amounts up to USD 10,000 can be deposited at any time after returning. Amounts above USD 10,000 , which require a customs declaration on Form FMJ obtained at the port of entry , must be deposited within 30 days of arrival.

Can I open multiple RFCD accounts?

A customer can open multiple RFCD accounts at the same bank, but each must be in a different foreign currency , for example, one in USD and one in GBP. According to regulations and specific bank policies (such as Eastern Bank PLC and others),

Can non-residents open an RFCD account?

No. RFCD accounts are available only to persons ordinarily resident in Bangladesh. Non-resident Bangladeshis should open an NFCD account instead.

The information in this article is provided for general informational and educational purposes only and does not constitute financial, legal, or tax advice from nsave or any of its affiliates. It is not a substitute for advice from a qualified financial advisor. We make no representations or warranties, whether expressed or implied, that the content is accurate, complete, or up to date.

Fees, exchange rates, incentives, and product availability may change and can vary by user and jurisdiction. Examples are illustrative only. Before making any financial decisions, seek advice from a qualified financial advisor who can assess your individual circumstances and objectives.

nsave helps freelancers and professionals from Bangladesh, Nigeria, Pakistan, Egypt, and beyond receive and manage USD abroad. As a non-bank payment provider, your money is not protected by the Financial Services Compensation Scheme (FSCS).