NPSB Bangladesh: What It Is, How It Works, and When to Use It

In November 2025, Bangladesh Bank expanded NPSB to allow instant transfers between any bank account, bKash wallet, Nagad wallet, or payment service provider in the country , a change that affects every Bangladeshi with a bank account or mobile wallet. This guide is for anyone who has seen "NPSB" on their internet banking app, ATM screen, or bKash transaction history and wants to understand what it actually means. By the end, you will know what NPSB is, how it differs from BEFTN and RTGS, what it costs, and when to use each system.

What Is NPSB?

NPSB (National Payment Switch Bangladesh) is the central payment network that connects banks, mobile financial service providers such as bKash and Nagad, and payment processors across Bangladesh for real-time retail transactions.

Owned and operated by Bangladesh Bank, NPSB functions like a roundabout in the middle of Bangladesh's financial system: every interbank transaction enters the switch, gets routed to the right destination, and exits in real time. Without it, your DBBL card would only work at DBBL ATMs. With it, your card works at any connected ATM in the country.

According to financial reports from The Daily Star, following the suspension of the "Binimoy" platform in mid-2025 (August 2025) due to irregularities and contract breaches, the National Payment Switch Bangladesh (NPSB) has become the primary technical infrastructure for all interoperable digital transactions in the country.

NPSB currently connects 53 banks for ATM transactions and 50 banks for POS terminal payments. According to Bangladesh Bank's Payment Systems Department (PSD Circular No. 12, dated 13 October 2025), a directive expanded NPSB to enable direct transfers between bank accounts, bKash wallets, Nagad wallets, and payment service providers such as Upay starting in November 2025.

How NPSB Works

When you use another bank's ATM, pay at a merchant POS terminal with your debit card, or transfer money via internet banking to a different bank, your transaction travels through the NPSB switch in real time.

The NPSB flow works in five steps:

- You initiate a transaction , an ATM cash withdrawal, POS payment, or IBFT (Internet Banking Fund Transfer) via your bank's mobile or internet banking app.

- Your bank sends the transaction request to the NPSB switch.

- NPSB identifies the receiving institution and routes the instruction.

- The receiving institution confirms and the transaction settles instantly for savings and current accounts. Card-based transactions settle on the next business day.

- Both institutions receive settlement confirmation from NPSB.

NPSB does not physically move cash between banks in real time. It sends payment instructions. Actual settlement between banks happens through Bangladesh Bank's central accounts. This is why a transfer can appear instant to you even though no physical funds moved at that moment.

Two-factor authentication , usually an OTP sent to your registered mobile number , is mandatory for all NPSB-connected banks for internet banking, e-commerce, and card-not-present transactions. This is Bangladesh Bank policy, not each bank's individual choice.

For example, if you send money from your City Bank account to a bKash wallet via internet banking, your City Bank app sends the instruction to NPSB, NPSB routes it to bKash, and the funds appear in the recipient's bKash wallet , typically within seconds.

What NPSB Does

NPSB covers four core transaction types: ATM cash withdrawal at another bank's ATM, ATM fund transfer, POS card payments at merchant terminals, and Internet Banking Fund Transfer (IBFT) between accounts at different banks. As of November 2025, it also covers interoperable transfers between bank accounts and mobile wallets including bKash, Nagad, and Rocket.

ATM cash withdrawal: You can use any debit card at any NPSB-connected ATM, regardless of which bank owns the machine. The Maximum fee is BDT 20 per withdrawal, charged to the card issuer.

ATM fund transfer: You can transfer money from your account to another bank's account directly from an ATM, using the recipient bank's 6-digit bank code. Free for savings and current account transfers.

Balance inquiry and mini statement: You can check your balance or view a short transaction history at any NPSB-connected ATM. Maximum fee: BDT 5 each.

IBFT (Internet Banking Fund Transfer): You can transfer money from your account to a different bank's account via your bank's internet banking portal or mobile app. Maximum fee: BDT 10 per transfer. Funds arrive instantly for savings and current accounts.

POS card payments : You can pay at any NPSB-connected POS terminal using a debit card from any member bank. No charge to the customer. Merchants pay a minimum 1.6% Merchant Discount Rate (MDR), of which 1.1% goes to the card-issuing bank as an interchange fee. Bangladesh Bank explicitly prohibits passing any portion of this MDR to the customer.

Interoperable MFS and bank transfers (from November 2025) , send money directly between any combination of bank account, bKash wallet, Nagad wallet, Rocket wallet, or payment service provider such as Upay.

Which Banks Are Connected to NPSB in Bangladesh?

As of March 2026, 54 banks are connected to NPSB for ATM transactions and 50 banks for POS terminal payments. Bangladesh Bank has mandated that all scheduled banks participate, meaning every bank licensed to operate in Bangladesh is required to connect to NPSB.

The following banks are among the primary members connected to the NPSB network:

Major Commercial & Private Banks

As of March 2026, there are 12 Major Commercial & Private Banks connected to NPSB:

- Dutch-Bangla Bank Limited (DBBL)

- BRAC Bank Limited

- The City Bank Limited

- Eastern Bank Limited (EBL)

- Dhaka Bank Limited

- Islami Bank Bangladesh Limited (IBBL)

- Mutual Trust Bank Limited (MTB)

- Prime Bank Limited

- Bank Asia Limited

- United Commercial Bank Limited (UCB)

- Pubali Bank Limited

- Southeast Bank Limited

State-Owned & Specialised Banks

- Sonali Bank Limited

- Janata Bank PLC

- Agrani Bank Limited

- Rupali Bank Limited

- Bangladesh Krishi Bank

- Bangladesh Development Bank Limited (BDBL)

Foreign Commercial Banks

- Standard Chartered Bank

- HSBC

- Commercial Bank of Ceylon

- Woori Bank

- State Bank of India (SBI)

Other Notable Members

- Al-Arafah Islami Bank

- Social Islami Bank Limited (SIBL)

- EXIM Bank Limited

- Jamuna Bank Limited

- Mercantile Bank Limited

- One Bank Limited

- NRB Commercial Bank

- Community Bank Bangladesh

NPSB Transaction Limits and Charges

As of 2026, Bangladesh Bank guidelines allow individual users to transfer up to BDT 300,000 per transaction with a daily cap of BDT 1,000,000 over a maximum of 10 transactions. (Corporate limits are even higher at BDT 500,000 per transaction).

While the November 2025 mandate standardised the framework and fees for interoperable transactions, as of March 2026, it did not create a single, universal transaction limit for all users. This means interoperable transfer limits are not universal and are set by each institution based on the account type. Hence, each bank (like BRAC Bank), MFS (like bKash), and PSP (like Upay) sets its own interoperability ceilings based on the specific type of account held by the customer.

The interoperability fee structure, confirmed by PSD Circular No. 12 (October 2025), runs as follows:

According to Bangladesh Bank, a mandatory requirement for all interoperable transactions is that the applicable fee/charge amount must be displayed to the customer (sender) before the transaction is executed, and must be deducted from the sender's account. No fee can be collected from the recipient.

These are Bangladesh Bank maximum rates. Individual banks and MFS providers charge within these caps. Always check your institution's schedule of charges before initiating a transfer.

NPSB vs BEFTN vs RTGS

NPSB, BEFTN, and RTGS are all Bangladesh Bank-operated interbank payment systems , the difference is speed, transaction size, and availability.

NPSB operates in real-time, 24 hours a day including weekends and public holidays, with no minimum transaction amount. Transfers are capped at BDT 50,000 per transaction and BDT 5,00,000 per day, with a flat fee of BDT 10 per IBFT transfer, making it well-suited for everyday transfers between personal bank accounts, merchant payments, and cash withdrawals at any NPSB-connected ATM.

If you don't need the money delivered instantly, BEFTN is often the better choice. It's free, as Bangladesh Bank mandates zero charge, and your internet banking portal will show BDT 0.00 on the confirmation screen before you send. BEFTN usually delivers to the recipient's account by the next working day, and if you submit before 10:00 am, it often clears the same day.

NPSB is real-time and works 24/7, but it comes with two downsides most people don't mention. Many banks charge a flat BDT 10 fee for the real-time processing, and if there's a network glitch between the two banks during peak hours, your transfer can get stuck in a pending state for up to 72 hours, the balance already deducted, requiring manual reconciliation to resolve.

That's the risk you're taking for speed. So the practical suggestion is: use BEFTN as your default for large transfers, bill payments, or anything that can wait until the next day. Use NPSB only when the transfer genuinely cannot wait.

BEFTN (Bangladesh Electronic Funds Transfer Network) is batch-processed , not instant. Transfers submitted before the cut-off on a working day process the same day; transfers submitted after cut-off or on Friday, Saturday, or public holidays process the next working day. Bangladesh Bank mandates the network itself is free. However, individual banks apply their own portal service charges. As of March 2026, Islami Bank lists the EFT charge as free in their Schedule of Charges but applies a separate BDT 10 iBanking portal fee per transaction , both are technically true at once.

BEFTN is best for: salary disbursement, vendor payments, and bulk or scheduled transfers where same-day processing is acceptable.

RTGS (Real Time Gross Settlement) is designed exclusively for high-value, time-critical transfers, with a minimum transaction amount of BDT 1,00,000, a personal daily limit of BDT 5,00,000, and a flat fee of BDT 100 per transaction. Processing is available on business days only no weekends or public holidays, with a 5:00pm cut-off for BDT transactions (branch counters close at 4:00pm, after which only internet banking and mobile app transfers are accepted); foreign currency RTGS closes at 4:00pm.

According to Bangladesh Bank's operational guidelines for the BD-RTGS system, a valid payment is considered final and irrevocable once it has been accepted and processed by the central system. RTGS is not just a large-value transfer channel for individuals, it is the same infrastructure used for government securities settlement and interbank foreign currency transactions, making it institutional-grade infrastructure repurposed for retail use rather than a faster version of NPSB.

NPSB is how money moves inside Bangladesh's banking system. For anyone receiving income from abroad , freelancers, remote workers, or professionals with international clients , the money has to arrive somewhere first. Where it lands, and what it earns while it sits, determines how much actually reaches your local bank account.

How to Receive International Payments and Convert to BDT with nsave

To receive international payments and convert them to BDT, open a nsave USD account, direct your foreign income to it using your personal ACH routing number and account number, and initiate a local currency withdrawal to your Bangladeshi bank account or bKash when ready.

Step 1: Open Your nsave USD Account

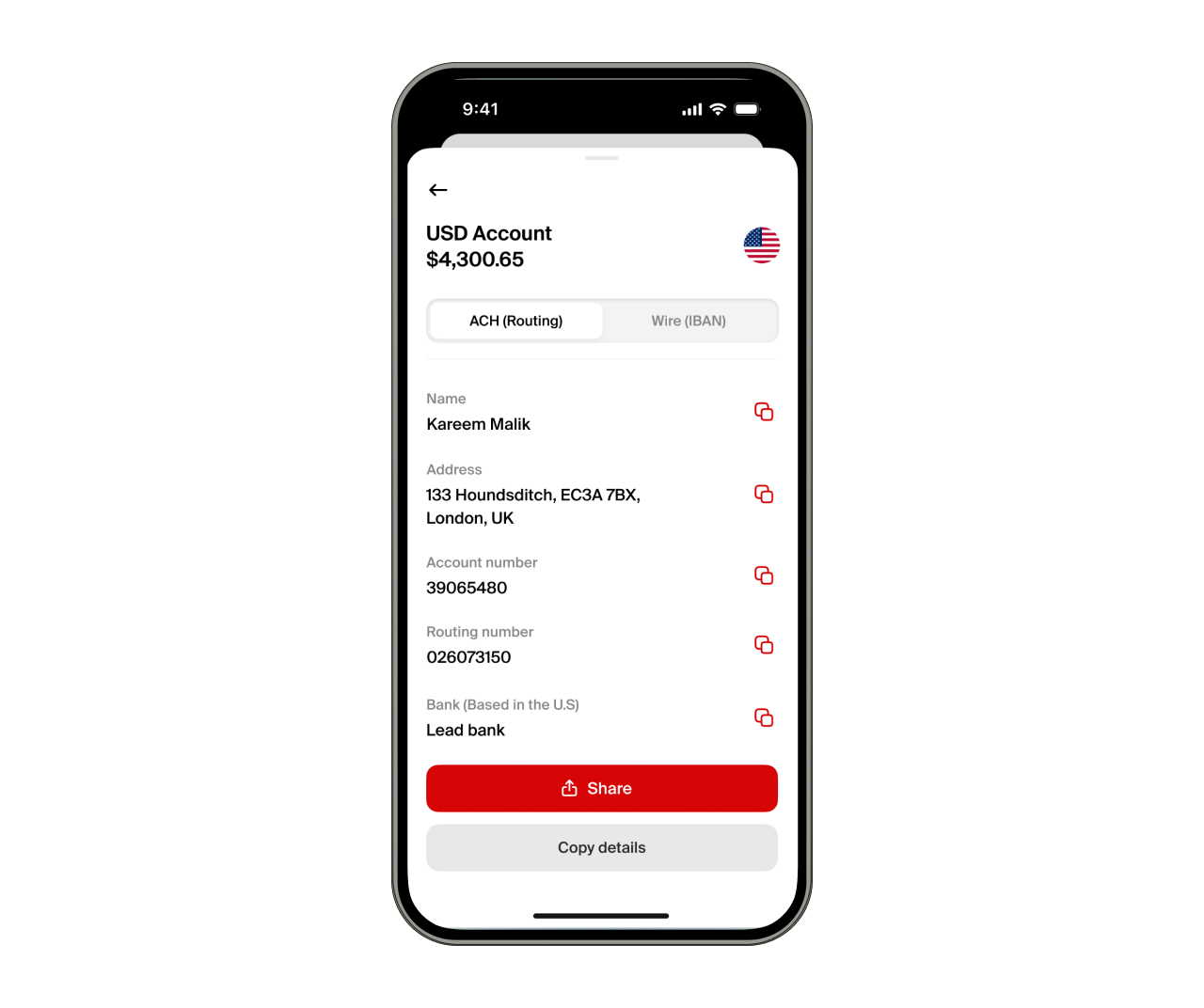

To open a nsave USD account, download the nsave app and complete identity verification using your passport or national ID , the process takes under 10 minutes. The Standard plan costs $0 per month (check the nsave app as fees are subject to change). Once verified, nsave assigns a personal US ACH routing number and account number. No branch visit required. No physical card required to get started.

Step 2: Direct Your Foreign Income to nsave

To receive foreign income via nsave, share your ACH routing number and account number with the platform or client paying you. Any platform that can pay a US bank account , including Upwork, Fiverr, Toptal, Deel, PeoplePerHour, Freelancer.com, Payoneer, and Wise , can send funds directly to your nsave account. Receiving via ACH or SWIFT is free on both Standard and Pro plans (check the nsave app as fees are subject to change)

Step 3: Convert and Send to Your Local Account or bKash

To convert USD to BDT, initiate a local currency withdrawal in the nsave app. The app displays the exact BDT amount before you confirm. Minimum payout fee: $1 (confirm on nsave app as fees may change). Funds arrive in your Bangladeshi bank account or bKash. The conversion rate and fee are shown upfront , no hidden charges.

Can I Use Wise to Receive International Payments in Bangladesh?

As of March 2026, according to the Wise Help Center, Wise is available in Bangladesh primarily for receiving money from abroad via bank transfer, bKash, or Nagad. While you can send BDT to Bangladesh, full, unrestricted access to create new, fully verified personal accounts from within Bangladesh has become limited for new users.

Can I Use Payoneer to Receive and Convert International Payments?

Yes, Payoneer is widely used in Bangladesh for receiving freelance income and converting to BDT via bank withdrawal.

NPSB and International Payments

For Bangladeshis receiving income from abroad, NPSB is the final leg of the journey , it moves BDT between local bank accounts once funds have already arrived in Bangladesh. The question is what happens before that: where does the foreign income land, and how much is lost before it reaches a local account?

NPSB is excellent for moving money inside Bangladesh. For receiving it from outside, the platform you choose first determines what is left to move.

confirm rates and fees on nsave app as fees and reward rates may change.

Key Takeaways

NPSB , National Payment Switch Bangladesh , is the Bangladesh Bank-operated network that enables real-time interbank transactions: ATM withdrawals at any NPSB-connected bank, POS payments at merchant terminals, and IBFT transfers between different bank accounts. It connects 53 banks for ATM transactions and, as of November 2025, enables direct transfers between bank accounts and mobile wallets including bKash and Nagad.

For everyday transactions, NPSB is the right tool: instant, available 24/7, low-fee (maximum BDT 10 for IBFT, BDT 20 for ATM withdrawals), and accessible at any connected ATM or via internet banking. BEFTN handles bulk or scheduled payments such as salary disbursement, with zero network fee and same/next business day processing. RTGS handles high-value, time-critical transfers above BDT 1,00,000 at BDT 100 per transaction , and once processed, cannot be reversed.

For income arriving from outside Bangladesh , via Upwork, Fiverr, or international clients , NPSB does not apply. A nsave USD account receives that income first, earns rewards while you hold it (confirm on nsave app for current rates , and converts to BDT for onward transfer via your local bank or bKash with a minimum $1 fee (confirm on nsave app as fees may change).

The information in this article is provided for general informational and educational purposes only and does not constitute financial, legal, or tax advice from nsave or any of its affiliates. It is not a substitute for advice from a qualified financial advisor. We make no representations or warranties, whether expressed or implied, that the content is accurate, complete, or up to date.

Fees, exchange rates, incentives, and product availability may change and can vary by user and jurisdiction. Examples are illustrative only. Before making any financial decisions, seek advice from a qualified financial advisor who can assess your individual circumstances and objectives.

nsave helps freelancers and professionals from Bangladesh, Nigeria, Pakistan, Egypt, and beyond receive and manage USD abroad. As a non-bank payment provider, your money is not protected by the Financial Services Compensation Scheme (FSCS).