Income Tax in Bangladesh (Rates, Filing, and What Freelancers Need to Know)

Most Bangladeshis filing a return this year have noticed something without being able to name it: the 5% slab is gone. The first taxable bracket now starts at 10%. The tax-free threshold went up slightly but if your income is between BDT 375,000 and BDT 475,000, you pay more tax in FY 2025–26 than you did a year ago, even though earnings stayed the same.

This guide covers who that affects, what the current rates are, whether you need to file, how to file online through etaxnbr.gov.bd, and the specific rules that apply to freelancers and remote workers earning income from international clients.

The Bangladesh Income Tax System

As of March 2026, Bangladesh uses a progressive income tax system, meaning the rate you pay increases as your income rises, with different portions of your income taxed at different rates, not your entire income at the top rate.

The National Board of Revenue (NBR) , restructured in 2025 into the Revenue Policy Division and Revenue Management Division, manages income tax collection and enforcement. The income year runs from 1 July to 30 June. The assessment year begins immediately after. Tax slabs apply to the income you earn during the income year, but you file your return during the following assessment year. Hence, filing for income year 2025–26 happens in the assessment year 2026–27.

Income Tax Rates for FY 2025–26

For the income year 2025–26 (assessment year 2026–27), the tax-free threshold for general taxpayers is BDT 375,000, and the first taxable slab starts at 10% , the 5% bracket has been removed.

Special Higher Tax-Free Thresholds

4 categories of taxpayers qualify for higher tax-free income thresholds under Bangladesh's income tax rules:

- Women and senior citizens (age 65 and above): BDT 425,000

- Persons with disabilities and third gender individuals: BDT 500,000

- Guardians of persons with disabilities: BDT 475,000

- War-wounded freedom fighters and July Warriors 2024: BDT 525,000

The removal of the 5% slab creates a specific impact on mid-range earners. Under the old rules (where the threshold was BDT 350,000), a person earning BDT 450,000 had their remaining BDT 100,000 taxed at a flat 5%, totaling BDT 5,000. Today, the tax-free threshold is higher at BDT 375,000, but the remaining BDT 75,000 is taxed at 10%, totaling BDT 7,500. The same income costs BDT 2,500 more this year. That difference compounds at higher incomes.

For example, if your annual income is BDT 700,000, the first BDT 375,000 is tax-free. The next BDT 300,000 is taxed at 10% (BDT 30,000). The remaining BDT 25,000 is taxed at 15% (BDT 3,750). Total tax payable: BDT 33,750, before accounting for any investment rebates.

Before filing your tax, ensure you confirm current slabs at etaxnbr.gov.bd or with a registered tax consultant before filing.

What are the Minimum Income Tax Rules in Bangladesh?

If your income exceeds the tax-free threshold, a minimum tax of BDT 5,000 applies for AY (Assessment Year) 2026–27, regardless of how low your slab-calculated tax works out.

The minimum tax is a floor, not an addition. If the slab calculation produces a tax figure below BDT 5,000, you pay BDT 5,000 instead. For new taxpayers registering for the first time, the minimum is BDT 1,000. According to the Finance Ordinance 2025 as outlined by LegalSeba, a standard minimum income tax of BDT 5,000 applies nationwide for individuals exceeding the tax-free threshold, removing the previous location-based tiers.

Who Must File an Income Tax Return in Bangladesh?

In Bangladesh, you must file an income tax return if your income exceeds the tax-free threshold , but certain categories must file even if their income is below it.

Categories that must file regardless of income level in Bangladesh includes:

- Salaried employees of companies whose employers require a TIN for payroll processing.

- Self-employed individuals and freelancers , once a TIN exists, annual filing is mandatory.

- Company directors and firm partners.

- Individuals previously assessed for tax.

- Anyone required to submit a Proof of Return Submission (PSR) for specific transactions, including opening a bank account above certain deposit thresholds, obtaining a trade licence, and purchasing sanchaypatra (government savings certificates).

The common misconception is that below-threshold earners don't need to file. If you hold a TIN, you file ,even if your total tax liability is zero. This applies directly to freelancers who obtained a TIN for banking purposes and then assumed no obligation followed.

Investment Tax Rebates in Bangladesh

To reduce your tax liability in Bangladesh, you can invest in approved instruments before the end of the income year (30 June). The rebate is calculated as 15% of your allowable investment, but it is subject to a strict "lower of" cap.

The Three-Way Cap Rule

Even if your individual investments are below the caps above, the NBR (National Board of Revenue) still applies a triple-limit check on the total rebate amount. The final tax rebate you receive will be the lowest of these three:

- 3% of your total taxable income (excluding certain types like capital gains).

- 15% of your actual "allowable" investment.

- A fixed maximum limit of BDT 10 Lakh (reduced from BDT 15 lakh in older acts)

Approved Investment Instruments and Individual Rebate Limits

The NBR (National Board of Revenue) recognises 5 major investment instruments for the annual tax rebate calculation. Investing beyond these caps is permitted, but only the amounts below count toward the rebate:

- Sanchaypatra (National Savings Certificates): Capped at BDT 5 lakh per year.

- DPS (Deposit Pension Scheme): Capped at BDT 1.2 lakh per year.

- Listed shares and mutual funds: Capped at BDT 5 lakh per year.

- Life insurance premiums: Capped at 10% of the policy's face value.

- Provident Fund: Both employee and employer contributions count in full, no separate cap stated.

Filing Deadline Requirement

The investment rebate applies only if you file your tax return by Tax Day. A late return or approved extension forfeits the entire rebate for that year, the full tax liability applies as if no qualifying investments were made.

Tax Rules for Freelancers and Remote Workers in Bangladesh

Freelancers in Bangladesh are treated as self-employed individuals and must pay income tax on earnings above the tax-free threshold , but two important exemptions reduce or eliminate the amount owed for most tech and IT workers.

Exemption 1: IT and technology services income

According to the Finance Act 2024, Income from IT and technology-based services earned between 1 July 2024 and 30 June 2027 is fully exempt from income tax , provided the full amount is received via bank transfer. Services covered under this exemption include software development, digital marketing, graphic design, content writing, data processing, and similar technology-based work. If income is received in cash or through an informal channel, the exemption does not apply. The bank transfer requirement is the condition, not the type of service alone.

Exemption 2: Foreign income legally remitted to Bangladesh

Income earned by a Bangladeshi citizen and legally remitted to Bangladesh through an authorised channel is exempt from income tax. This exemption is widely misunderstood. Many freelancers who earn USD from international clients and receive the funds through a Bangladeshi bank account or authorised remittance service are not taxable on that income in Bangladesh , subject to NBR conditions.

What freelancers must do regardless of exemptions:

- Register for an e-TIN at etaxnbr.gov.bd

- File an annual income tax return , even if total tax owed is zero

- Declare all income sources, including foreign earnings, in the return

VAT: Export of services to foreign clients is zero-rated under Bangladesh's VAT law, VAT does not apply if payment is received in foreign currency. This is separate from income tax.

For example, if you earn $10,000 from Upwork in FY 2025–26, receive the full amount via your Bangladeshi bank account, and the income qualifies as IT/tech services, your income tax liability on that income is zero , but you still need a TIN and must file your return.

Note: A Freelancer ID card is generally not mandatory just to receive foreign income into a standard savings account. Banks like Standard Chartered and Eastern Bank (EBL) often list the Freelancer ID as a requirement or a preferred document to open dedicated "Freelancer Suite" accounts, which offer benefits like ERQ (holding USD) and specialised credit cards.

An employer appointment letter, contract, or marketplace work order is typically sufficient to satisfy Central Bank "Source of Fund" requirements. However, for large or frequent transfers, banks may still request a Freelancer ID to ensure the funds qualify for government incentives like the 2.5% government remittance incentive.

How to File Your Income Tax Return Online in Bangladesh

To file your income tax return in Bangladesh, go to etaxnbr.gov.bd, log in with your e-TIN and biometrically verified phone number, complete the return form, and submit before 30 November of the assessment year.

Step 1: Get Your e-TIN

Your TIN registration starts at etaxnbr.gov.bd. Enter your National ID number to register. Your TIN is issued immediately on completion. It is required for all subsequent filings and for many financial transactions including bank account upgrades, trade licences, and sanchaypatra (National Savings Certificates) purchases.

Step 2: Gather Your Income Information

You do not need to upload supporting documents for the return, but you must have the numbers ready. Collect:

- Total income from all sources: salary, freelance earnings, rental income, interest, capital gains

- Total investments in approved instruments for the rebate calculation

- Bank balances and asset details for the wealth statement section

Keep your records and bank statements on file. NBR can request verification documents separately.

Step 3: Log In and Complete the Return Form

Go to etaxnbr.gov.bd. Log in with your TIN and password. First-time filers must have a biometrically verified mobile number , the SIM must be registered to your NID through the biometric verification your mobile operator completed at the time of SIM activation. Select the relevant income year. Enter each income category, declare foreign earnings, and claim your investment rebate. The portal calculates the tax automatically.

Step 4: Pay Tax and Submit

If tax is owed, pay via the portal's online payment system or through a designated bank before submitting the return. Keep the payment challan as proof. Submit the return, then download your acknowledgement receipt, the PSR (Proof of Submission of Return). This document is required for a wide range of financial transactions including bank account applications, trade licences, and savings certificate purchases.

What Happens If You Miss the Deadline?

Missing the tax return deadline in Bangladesh triggers two immediate consequences: a financial penalty and the automatic loss of your investment tax rebate.

The penalty differs based on your filing history. New taxpayers pay the higher of 10% of tax payable or BDT 5,000, while previously assessed taxpayers pay the higher of 50% of last assessed tax or BDT 1,000. On top of the fine, 4% monthly interest accrues on any unpaid tax for every month of delay.

The rebate forfeiture is often the costlier consequence. Filing even one day late voids 100% of your investment tax credit — meaning any rebate expected from a DPS, Sanchaypatra (National Savings Certificates), or life insurance contribution is completely lost, and full tax becomes payable as if no investment was made.

Late filing also raises audit risk. A mismatch between TDS records from your bank or employer and your late submission can trigger a manual review. For freelancers, this is especially significant; income received in USD through official banking channels may qualify as tax-exempt, but that exemption requires timely filing. A late return can cause exempt foreign income to be reclassified as unexplained wealth, taxable at the highest applicable rates.

For most salaried employees, income flows through one employer and one bank account. For freelancers and remote workers, income arrives in USD from multiple international clients, sits in different accounts, and converts at different rates on different days. How that income arrives in Bangladesh determines what you can declare, which exemptions apply, and how much BDT you actually end up with after conversion. That makes the receiving account a tax consideration as much as a payment decision.

For Bangladeshi freelancers and remote workers, tax compliance starts with the income year, but the real financial impact happens before the return is filed, at the moment USD earnings are received and converted to BDT. Where that USD sits, what rate it converts at, and whether it qualifies for the IT/tech exemption all depend on how and where the funds arrive. Structuring that receiving setup correctly keeps more of what you earn.

How to Receive USD Freelance Income and Convert to BDT

To receive USD freelance income from international clients and convert it to BDT at a chosen time, open a nsave USD account, share your ACH details as your payout destination, and initiate a BDT withdrawal when you are ready.

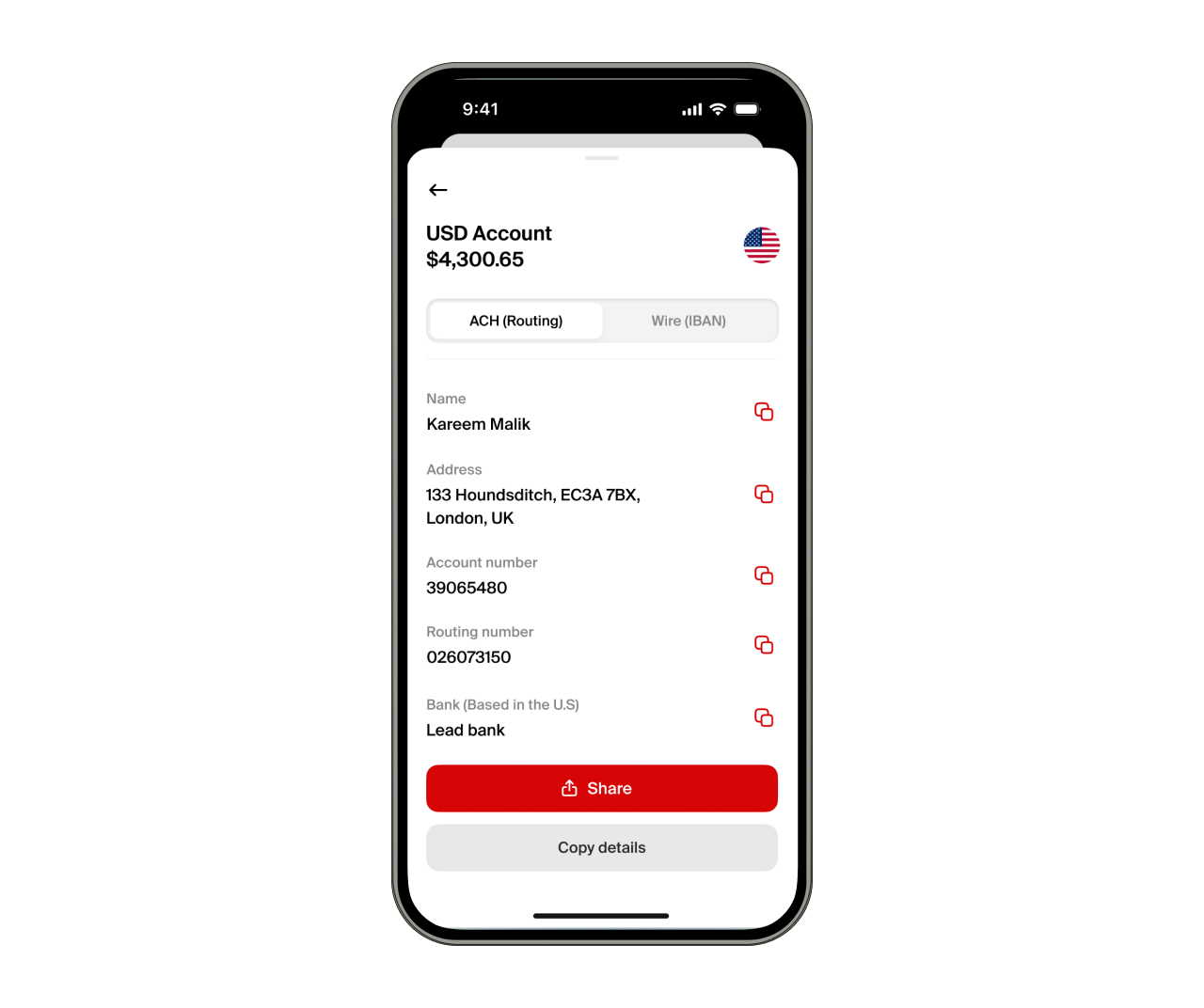

Step 1: Open Your nsave USD Account

Your nsave account is free on the Standard plan ($0/month). Download the nsave app, complete identity verification using your passport or national ID , takes under 10 minutes, no branch visit. Once verified, nsave assigns a personal ACH routing number and account number, which any international client or platform can use to pay you directly in USD.

Step 2: Set nsave as Your Payout Destination on Your Earning Platforms

To receive USD via nsave, share your ACH routing number and account number as the withdrawal destination on Upwork, Fiverr, Toptal, Freelancer.com, PeoplePerHour, or Deel. Direct clients paying via SWIFT can use nsave's wire details instead. Receiving funds via ACH or SWIFT is free on both Standard and Pro plans. The USD arrives in your nsave account unconverted, you control when the conversion happens.

Step 3: Convert to BDT and Send to Your Bangladeshi Local Account

To convert USD to BDT, initiate a local currency withdrawal in the nsave app. The exact BDT amount is shown before you confirm. Minimum transfer fee is $1 (fees subject to change, check the nsave app for current rates). Funds arrive in your Bangladeshi bank account.

To qualify for Bangladesh's IT/tech income tax exemption, freelance earnings must be received via bank transfer. A nsave USD account is a non-resident USD account, ensure that the final BDT transfer from nsave to your Bangladeshi bank account is documented as an inward remittance in your records for NBR purposes. Consult a registered tax consultant before declaring nsave-received USD income in your return if you are uncertain of the correct classification.

nsave is not a bank. Funds held in nsave are not FSCS-protected.

Key Takeaways

Bangladesh uses a progressive tax system where the tax-free threshold for general taxpayers is BDT 375,000. The 5% tax slab has been removed; the first taxable bracket now starts at 10%, rising to 30% for the highest earners. A nationwide minimum tax of BDT 5,000 applies to any individual whose income exceeds the threshold

Filing an annual return at etaxnbr.gov.bd is mandatory for all TIN holders, including freelancers and self-employed individuals, regardless of whether tax is owed. According to a National Board of Revenue (NBR) directive reported by Bangladesh Sangbad Sangstha (BSS), the extended deadline for individual tax return submission for the current assessment year was March 31, 2026.. Filing after this date is a "Belated Return," which triggers an immediate BDT 5,000 penalty and the total forfeiture of your investment tax rebate.

The rebate is 15% of qualifying investments (e.g., DPS up to 1.2L, Sanchaypatra up to 5L), but it is strictly capped. Your rebate is the lowest of:

- 15% of your actual investment.

- 3% of your total taxable income.

- BDT 10 Lakh

So even if you invest heavily, the rebate you actually receive will never exceed BDT 10 Lakh, and may be far less depending on your income.

The information in this article is provided for general informational and educational purposes only and does not constitute financial, legal, or tax advice from nsave or any of its affiliates. It is not a substitute for advice from a qualified financial advisor. We make no representations or warranties, whether expressed or implied, that the content is accurate, complete, or up to date.

Fees, exchange rates, incentives, and product availability may change and can vary by user and jurisdiction. Examples are illustrative only. Before making any financial decisions, seek advice from a qualified financial advisor who can assess your individual circumstances and objectives.

nsave helps freelancers and professionals from Bangladesh, Nigeria, Pakistan, Egypt, and beyond receive and manage USD abroad. As a non-bank payment provider, your money is not protected by the Financial Services Compensation Scheme (FSCS).