BEFTN: What It Is, How It Works, and When to Use It (2026)

Most government salary payments and social safety net transfers in Bangladesh run through a system most people have never heard of by name: BEFTN. If you've seen "BEFTN Transfer" or "EFT" as an option in your bank's internet banking portal and skipped past it, this article is for you.

BEFTN , Bangladesh Electronic Funds Transfer Network , is Bangladesh Bank's primary batch-processing system for moving funds between bank accounts across different banks. It handles payroll for hundreds of thousands of government employees, utility bill collections, corporate vendor payments, and domestic personal transfers every working day.

By the end of this article you will know exactly how BEFTN works, what it costs, when to use it instead of NPSB or RTGS, what information you need to make a transfer, and how foreign income fits into the picture before it reaches the BEFTN network.

What is BEFTN?

BEFTN (Bangladesh Electronic Funds Transfer Network), is Bangladesh Bank's batch-processing system for transferring funds electronically between bank accounts at different banks within Bangladesh, launched on 28 February 2011.

BEFTN was Bangladesh's first paperless interbank fund transfer system. Bangladesh Bank operates it. Rather than physically moving cash or processing paper instruments such as cheques or demand drafts, BEFTN bundles payment instructions from multiple banks and settles them together in scheduled batches during the working day. The system handles 2 transaction directions:

- Credit transfers: money sent out from the sender's account to a recipient at a different bank , salary disbursements, vendor payments, personal transfers

- Debit transfers: money pulled from an account by a collecting entity , loan EMI collections, utility bill payments, insurance premium collections

According to Bangladesh Bank's Payment Systems Department (PSD Circular No. 06/2023), in November 2023, BEFTN was migrated to the Nikash-BEFTN framework under PSD Circular No. 06/2023, which consolidated Bangladesh Automated Clearing House (BACH) transfers. The Nikash-BEFTN system went live on 12 November 2023.

How BEFTN Works

To send money via BEFTN, the sender's bank collects the payment instruction, bundles it with other transactions in a batch, sends it to BEFTN for central processing, and the recipient's bank credits the account once settlement is confirmed.

Step 1: Origination (Sender's Bank)

The sender initiates a transfer at their bank , through internet banking, a mobile banking app, or at a branch , providing the recipient's account number, bank name, branch name, and the 9-digit routing number. The sender's bank , the Originating Bank , packages this as an EFT entry and forwards it to the BEFTN central system.

Step 2: Batch Processing (BEFTN Central System)

BEFTN operates in 3 sessions each working day: 12:00 am to 11:59 am, 12:00 pm to 2:59 pm, and from 3:00 pm. Each transaction completes within the 2 sessions following submission. The same-day cut-off time is 12:30 pm , any transfer submitted before this point on a working day is processed the same day. Transfers submitted after 12:30 pm, or on Friday, Saturday, or a public holiday, are processed on the next working day. The BEFTN return window is 2 sessions, not 2 calendar days.

Step 3: Settlement (Recipient's Bank)

Once BEFTN processes the batch, final settlement takes place through accounts held at Bangladesh Bank. The Receiving Bank gets the credit and posts it to the recipient's account. Settlement is multilateral , all participating banks' positions are calculated into a single net figure and settled simultaneously, rather than bank by bank.

For example, if your company submits a payroll batch for 200 employees across different banks before 12:30 pm on a Wednesday, all employees receive their salary credits in their respective bank accounts on the same day.

What BEFTN is Used For

BEFTN handles a wide range of credit and debit payment types , from salary and payroll disbursements to utility bill collections, dividend distributions, and government benefit payments.

Credit transfers (money sent out):

- Salary and payroll payments

- Domestic interbank remittances

- Company dividend distributions

- Government social safety net payments

- Expense reimbursements

- Corporate vendor payments

- Government tax and pension payments

Debit transfers (money pulled in):

- Mortgage and loan EMI collections

- Insurance premium collections

- Utility bill payments

- Association and club membership fees

Most government salaries and social benefit payments in Bangladesh are processed through BEFTN , it is core payment infrastructure, not an optional feature. For businesses, BEFTN is the standard mechanism for high-volume, scheduled payment runs where real-time settlement is not required.

BEFTN Charges and Transaction Limits

BEFTN transfers carry no Bangladesh Bank infrastructure fee , any charge applied is bank-specific and set at the individual bank's discretion, unlike RTGS which carries a flat fee of BDT 100 per transaction.

4 points on cost and limits:

- No central BEFTN fee: Bangladesh Bank mandates that the BEFTN network itself is free at the infrastructure level. However, individual banks apply their own portal or service charges. Sonali eWallet, for example, shows BDT 0.00 on the confirmation screen. Islami Bank, however, applies a separate BDT 10 iBanking service charge per BEFTN transaction , so the transfer itself is free but the platform fee is not. Check your specific bank's schedule of charges before assuming zero cost.

- Minimum transaction amount: Set by individual Banks.

- Bank-level daily limits: Limits vary by bank. At Islami Bank, as of March 2026, BEFTN supports up to BDT 5 lakh per day across 20 transactions. Sending the full BDT 5 lakh in a single transaction exhausts the daily ceiling immediately

- For context: RTGS carries a flat BDT 100 fee per transaction. NPSB at Islami Bank carries a flat BDT 10 fee per transaction for real-time transfers up to BDT 50,000

Bangladesh Bank mandates that the BEFTN network itself is free of charge at the infrastructure level. While it's technically correct, what it leaves out is that your bank can apply its own service charge for using their digital portal to initiate the transfer.

Islami Bank does exactly this. As of March 2026, their Schedule of Charges lists the EFT charge as free, but separately applies a BDT 10 iBanking service charge per transaction. So both things are true at once: the BEFTN transfer itself costs nothing, and the BDT 10 is a platform fee for using IBBL's iBanking portal. In practice, you pay BDT 10 to send a BEFTN transfer from Islami Bank, the distinction is just regulatory framing, not a real saving.

What You Need to Make a BEFTN Transfer

To make a BEFTN transfer, you need the recipient's bank account number, bank name, branch name, and the bank's 9-digit routing number; without the routing number, the transfer cannot be processed.

4 pieces of information are required:

- Recipient's full account number , exactly as held at the recipient's bank

- Recipient's bank name and branch name , the specific branch where the account is held

- The recipient bank branch's 9-digit routing number , a unique identifier issued by Bangladesh Bank for each bank branch in Bangladesh. Find it in 3 places: the Bangladesh Bank website publishes the full routing number directory; most banks print it on cheque books and bank statements; most internet banking portals display it in the account details section

- Transfer amount and payment reference , any transaction-specific reference the recipient needs for reconciliation

Most bank internet banking portals require a one-time password (OTP) or token passcode to authorise a BEFTN transfer. A single incorrect digit in the 9-digit routing number causes the transfer to fail or be directed to the wrong branch , and reversal after processing begins is difficult.

Note that different bank apps handle routing number entry differently. Unlike BRAC Bank's Astha or City Bank's CityTouch, which allow you to paste the 9-digit routing number directly, Sonali eWallet's BEFTN flow does not ask for a routing number upfront. In Sonali eWallet, the user selects a district first, then searches for the branch, and the routing number auto-fills as a read-only field after branch selection. If you don't know the exact official branch name, the Sonali eWallet flow can block progress.

How to Send a BEFTN Transfer via Internet Banking

To send a BEFTN transfer through internet banking, log into your bank's internet banking portal, select the external account transfer or BEFTN option, add the recipient as a beneficiary using their account and routing number, then initiate the transfer and confirm with your OTP or 2FA token.

Step 1: Log In and Navigate to Fund Transfer

Log into your bank's internet banking portal or mobile banking app. Locate the fund transfer section , labelled "External Transfer", "Interbank Transfer", or "BEFTN Transfer" depending on the bank.

Step 2: Add the Recipient as a Beneficiary

Select "Add Beneficiary" and enter: the recipient's full account number, the recipient's bank name, branch name, and the 9-digit routing number for that specific branch. Save the beneficiary , this information can be reused for future transfers to the same recipient without re-entering the routing number.

Note: as of March 2026, Islami Bank iBanking requires pre-registration of every destination account as a beneficiary before any EFT or NPSB transfer can be sent. Once a beneficiary is added at Islami Bank, it cannot be deleted for 20 days , a friction point for one-off payments to new recipients.

Step 3: Enter Transfer Details and Submit

Select the saved beneficiary account, enter the transfer amount, add a payment reference if required, and review all details before submitting. Confirm the transaction using your OTP or 2FA token. The transaction is queued for the next available BEFTN batch session.

Step 4: Confirm Timing

Submit before 12:30 pm on a working day for same-day credit. Community experience suggests that submissions before 10:00 am frequently clear the same day. Submissions after 12:30 pm, or on Friday, Saturday, or a public holiday, are processed on the next working day.

BEFTN vs NPSB vs RTGS

BEFTN, NPSB, and RTGS are all Bangladesh Bank-operated interbank payment systems, but they serve different purposes , BEFTN is for scheduled batch transfers, NPSB is for real-time card and account transactions, and RTGS is for high-value, instant gross settlement.

BEFTN vs NPSB

BEFTN processes transactions in batches at scheduled times and is designed for direct bank-to-bank credit and debit transfers , salary payments, vendor payments, personal transfers. NPSB processes card-based and internet banking fund transfers in real time. The practical distinction: BEFTN is for initiating a direct bank-to-bank transfer of funds; NPSB is used when the transaction originates from a debit card, credit card, ATM, POS terminal, or real-time interbank fund transfer. According to financial reports, following Bangladesh Bank's suspension of the Binimoy platform in August 2025 due to irregularities and contract breaches, NPSB became the primary technical infrastructure for all interoperable digital transactions in Bangladesh

If you don't need the money delivered instantly, BEFTN is often the better choice. It's free, as Bangladesh Bank mandates zero charge, and your internet banking portal will show BDT 0.00 on the confirmation screen before you send. BEFTN usually delivers to the recipient's account by the next working day, and if you submit before 10:00 AM, it often clears the same day.

NPSB is real-time and works 24/7, but it comes with two downsides most people don't mention. Many banks charge a flat BDT 10 fee for the real-time processing, and if there's a network glitch between the two banks during peak hours, your transfer can get stuck in a pending state for up to 72 hours, the balance already deducted, requiring manual reconciliation to resolve.

That's the risk you're taking for speed.

So the practical suggestion is: use BEFTN as your default for large transfers, bill payments, or anything that can wait until the next day. Use NPSB only when the transfer genuinely cannot wait.

BEFTN vs RTGS

Both BEFTN and RTGS handle bank-to-bank credit transfers, but they differ in speed, cost, and use case. BEFTN uses batch processing , same-day or next working day. RTGS settles each transaction individually in real time , within 30 minutes. RTGS carries a flat BDT 100 fee per transaction; BEFTN carries no central fee.

As of March 2026, RTGS operates under an asymmetric liability framework , the primary risk for instruction errors sits with the customer. An incorrect account or routing number in an RTGS payment is final and irrevocable once accepted by the central system; no reversal mechanism exists. For scheduled, non-urgent bulk transfers, BEFTN is more cost-effective and lower risk. For urgent, large-value payments where timing matters, RTGS is the right tool , with the caveat that every detail must be verified before submitting.

What are the Limitations of BEFTN?

The main limitations of BEFTN are that it is not real-time, it operates only on working days, and reversing a completed transaction is difficult.

4 practical limitations apply:

- Not instant: BEFTN batch processing introduces a delay between submission and settlement. For urgent payments, use RTGS instead

- Working day dependency: BEFTN does not process on Fridays, Saturdays, or public holidays. A transfer submitted Thursday afternoon is not processed until Sunday , the next Bangladesh working day

- Difficult reversal: Once a BEFTN payment enters the batch and settles, reversing it requires coordination between both the Originating Bank and the Receiving Bank , a process that takes time and is not guaranteed. Entering the correct account number and routing number before submitting is therefore non-negotiable

- Routing number precision: A single incorrect digit in the 9-digit routing number causes the transfer to fail, be delayed, or , in a worst-case scenario , credit the wrong branch account

These limitations matter most when the funds originate from outside Bangladesh. If your income arrives from abroad, from a foreign employer, a freelance platform such as Upwork or Fiverr, or a direct international client , it does not enter the BEFTN network to begin with. It arrives in a USD account first. What you do with it in that USD account, and how efficiently you eventually move it into your Bangladeshi bank account via a local payout, determines how much of it you actually keep.

How to Receive Foreign Income and Send It to Your Bangladeshi Bank Account

To receive USD income from a foreign employer, client, or freelance platform and transfer it to your Bangladeshi bank account, open a USD account with nsave , a global USD platform that provides personal ACH routing and account numbers for receiving international payments.

For Bangladeshi professionals earning in USD from abroad, BEFTN is the final leg of the journey , it's how funds move between Bangladeshi bank accounts once they've already been converted to Taka. The step before that matters just as much: how you hold and manage your USD before converting. The section below covers how to receive foreign income in USD, and move it to a Bangladeshi bank account when you're ready.

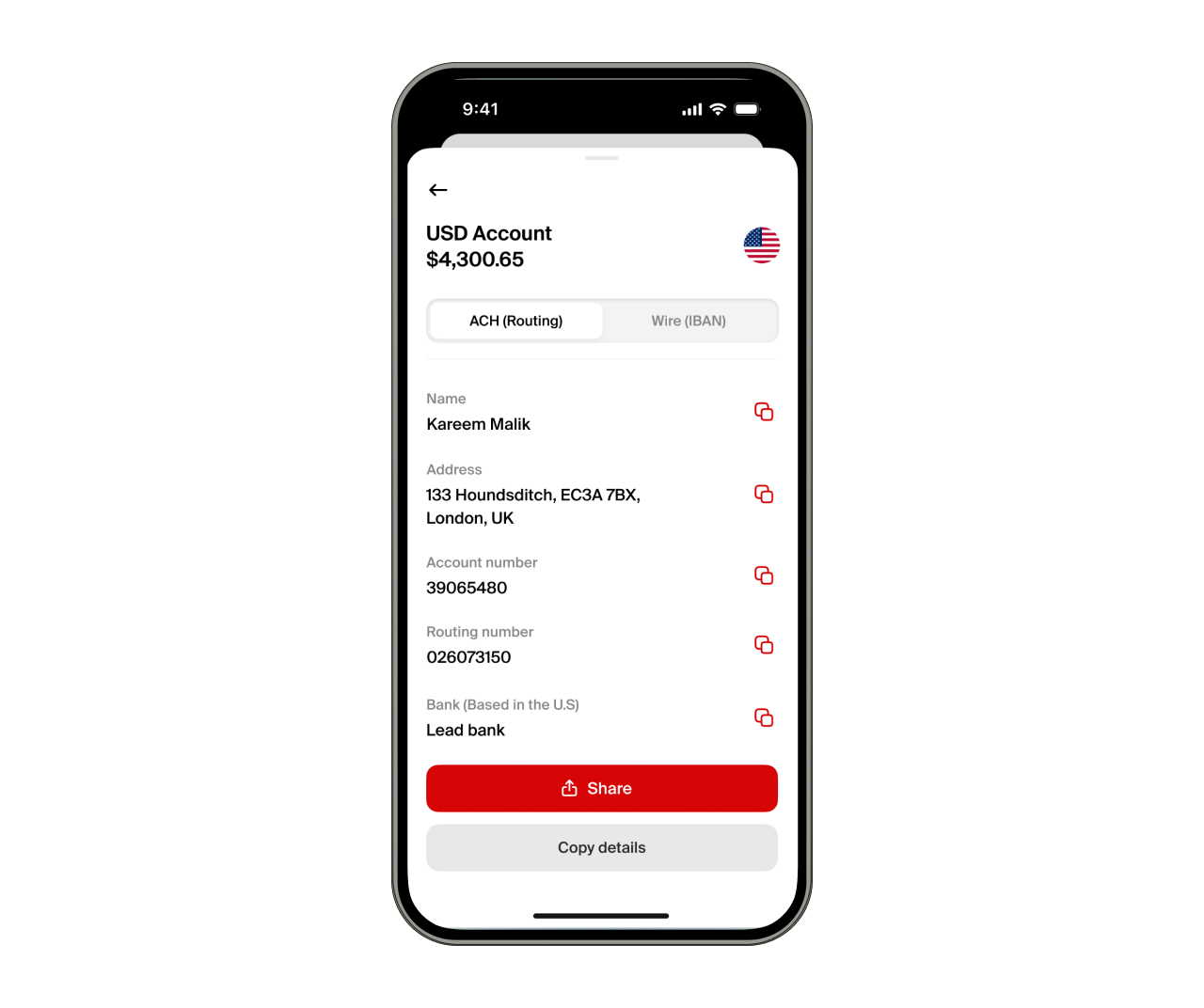

Step 1: Open Your nsave USD Account

To open a USD account with nsave, download the nsave mobile app and complete verification using your passport or national ID. The account opens in under 10 minutes with no branch visit required. The Standard plan carries no monthly fee (check the nsave app as fees are subject to change). Once verified, you receive a personal ACH routing number and account number, which you can share directly with Upwork, Fiverr, Toptal, Deel, PeoplePerHour, Freelancer.com, or any direct client or employer who pays via bank transfer.

New to nsave? Watch how to set up your account in under 10 minutes:

Step 2: Receive USD Payments

To receive payments, share your nsave ACH details as the withdrawal destination with any platform or client. Payments sent via ACH or international SWIFT wire transfer land in your nsave USD account. Receiving via ACH or SWIFT is free on both the Standard and Pro plans, no branch visit, no paper form.

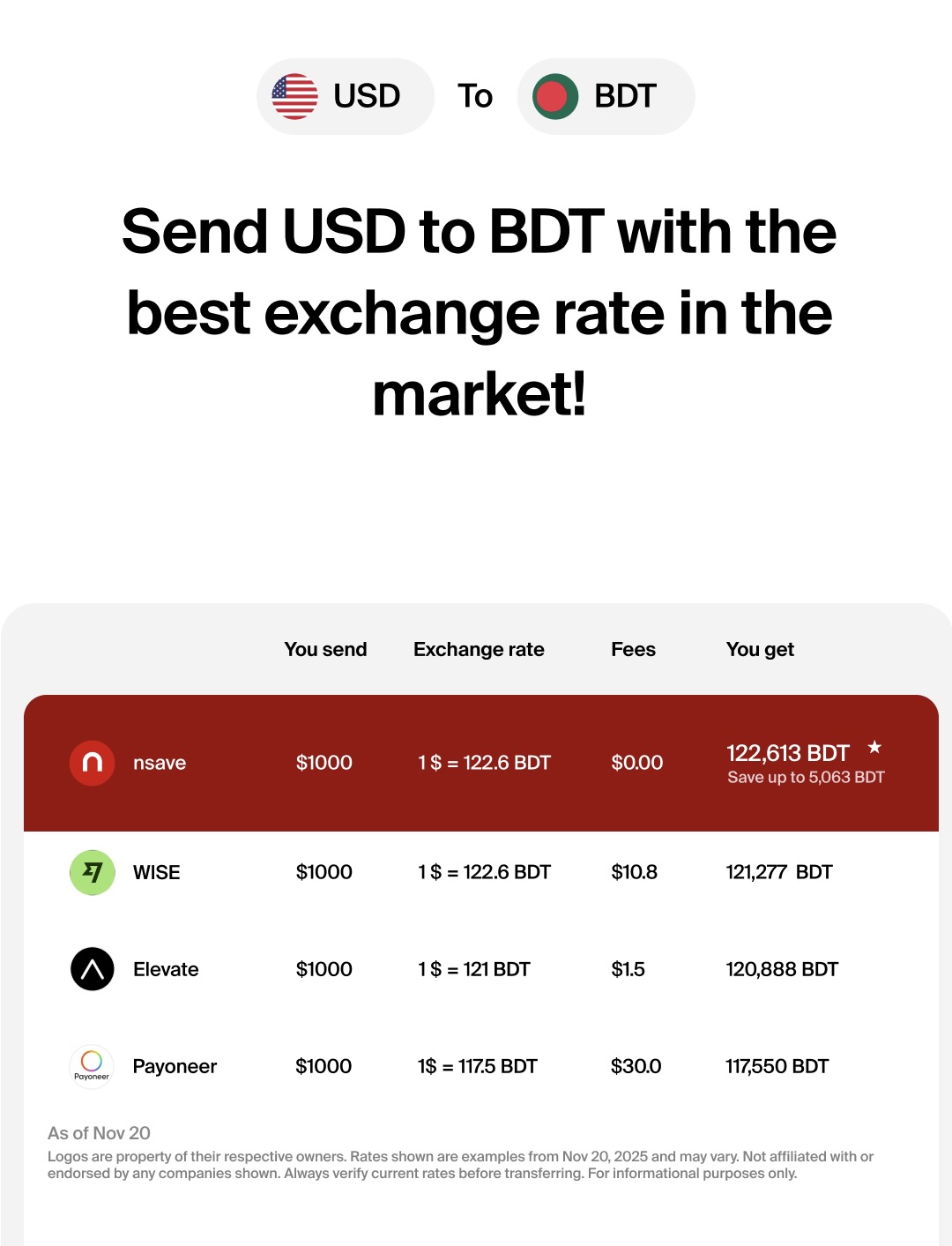

Step 3: Convert and Send to Your Bangladeshi Bank Account

To transfer to Bangladesh, initiate a local currency payout in the nsave app. The app shows the exact BDT amount before you confirm. The minimum payout fee is $1 (check nsave app as fees may change), and you transfer BDT to your local account. From there, any interbank movement within Bangladesh uses BEFTN or NPSB as normal.

Is Apple Pay Available in Bangladesh?

Apple Pay is not available in Bangladesh, local banks and card issuers do not support Apple Wallet integration, meaning Bangladeshi-issued cards cannot be added to Apple Pay for in-store, in-app, or online use. Apple Pay only functions in Bangladesh when paired with a foreign-issued card and a separate KYC setup, making it impractical as a primary payment method for local transactions.

Is Cash App Available in Bangladesh?

Cash App does not support Bangladeshi residents, the platform requires a US address, SSN or ITIN, and a US-based bank account to operate. Cash App cannot send funds to Bangladeshi bank accounts or bKash, and accounts created through VPNs or foreign numbers risk permanent suspension. Bangladeshi freelancers use nsave, Payoneer, ElevatePay, or PriyoPay as direct alternatives, all of which support USD receiving and local BDT withdrawal without residency requirements.

Is Wise Available in Bangladesh?

Yes, Wise is available in Bangladesh primarily for receiving money from abroad via bank transfer, bKash, or Nagad. While you can send BDT to Bangladesh, full, unrestricted access to create new, fully verified personal accounts from within Bangladesh has become limited for new users.

Key Takeaway

BEFTN is Bangladesh Bank's batch-processing interbank fund transfer system, launched on 28 February 2011 and migrated to the Nikash-BEFTN framework in November 2023. It processes salary payments, vendor payments, utility bill collections, dividend distributions, and government benefit transfers across all scheduled banks in Bangladesh. The same-day processing cut-off is 12:30 pm on working days. The BEFTN network carries no central fee, though individual banks apply their own portal charges.For urgent, real-time transfers, RTGS is the right system. For real-time card and ATM transactions, NPSB handles those. BEFTN is where bulk, scheduled, domestic interbank payments belong.

For professionals receiving foreign income from abroad, BEFTN is the final step , not the first. The step that matters more is how you hold and grow your USD before it converts to Taka. With nsave, that process happens in one app , from receipt to earning to payout to your Bangladeshi bank account.

Frequently Asked Questions

How long does a BEFTN transfer take?

BEFTN transfers typically process on the same day if submitted before the 12:30 pm cut-off time on a standard working day. If submitted after 12:30 pm, or on a Friday, Saturday, or public holiday, the funds will be credited to the recipient on the next working day.

What is the cut-off time for BEFTN?

The cut-off time for same-day processing is 12:30 pm. Transfers initiated after this time fall into the next batch session, which settles on the following working day.

What is a routing number and where do I find it?

A routing number is a unique 9-digit code assigned by Bangladesh Bank to identify a specific bank branch. You can find it on the Bangladesh Bank website's directory, printed on cheque books and bank statements, or within the account details section of most internet banking portals.

Is BEFTN free?

At the central infrastructure level, Bangladesh Bank mandates that BEFTN is free of charge. However, individual banks may apply their own platform or internet banking service fees (for example, a BDT 10 iBanking charge to initiate the transfer.

What is the minimum transfer amount for BEFTN?

There is no central minimum transfer amount mandated by Bangladesh Bank for BEFTN; you can send very small amounts. Limits are set by individual banks. (Note: RTGS, a different system, carries a strict BDT 100,000 minimum).

What happens if I enter the wrong routing number?

A single incorrect digit will cause the BEFTN transfer to fail, be significantly delayed, or in the worst-case scenario, be credited to the wrong branch. Because BEFTN operates in batches, reversing a processed error requires manual coordination between both banks, which is a difficult and slow process.

The information in this article is provided for general informational and educational purposes only and does not constitute financial, legal, or tax advice from nsave or any of its affiliates. It is not a substitute for advice from a qualified financial advisor. We make no representations or warranties, whether expressed or implied, that the content is accurate, complete, or up to date.

Fees, exchange rates, incentives, and product availability may change and can vary by user and jurisdiction. Examples are illustrative only. Before making any financial decisions, seek advice from a qualified financial advisor who can assess your individual circumstances and objectives.

nsave helps freelancers and professionals from Bangladesh, Nigeria, Pakistan, Egypt, and beyond receive and manage USD abroad. As a non-bank payment provider, your money is not protected by the Financial Services Compensation Scheme (FSCS).