Banks in Bangladesh: Types, Top Banks, and How to Choose

As of March 2026, Bangladesh has 62 scheduled banks but most people interact with fewer than five in their lifetime, and choosing the wrong one for your specific needs can cost you significantly in fees and friction. For freelancers receiving international USD, for salaried employees wanting reliable ATM access, and for small business owners comparing digital banking options, the difference between banks is not just branding. It is operational.

This guide covers how the Bangladesh banking system is structured, which banks lead in which categories, what to look for when opening an account, and how to set up the receiving infrastructure for international USD income.

How the Bangladesh Banking System Is Structured

Bangladesh's banking sector is regulated by Bangladesh Bank and consists of 62 scheduled banks divided into four main categories: state-owned commercial banks, private commercial banks, foreign commercial banks, and specialised development banks.

Bangladesh Bank is the central bank in Bangladesh and it sets monetary policy, issues licences, supervises all 62 scheduled banks, and manages the country's foreign exchange reserves. Scheduled banks are licensed under the Bank Company Act 1991 and authorised to offer the full range of banking services to the public.

The four categories serve distinct roles. State-owned banks serve public mandates and distribute widely across rural areas. Private commercial banks dominate retail banking, digital products, and SME lending. Foreign commercial banks serve corporate clients, multinational companies, and high-net-worth individuals. Specialised development banks focus on agricultural credit and industrial lending.

What are Types of Banks in Bangladesh?

As of March 2026, Bangladesh's 62 scheduled banks fall into four categories:

- State-owned commercial banks

- Private commercial banks

- Foreign commercial banks,

- Specialised development banks.

State-Owned Commercial Banks (SOCBs)

There are 7 SOCBs fully or majority-owned by the government. These are the oldest and most widely distributed banks by branch count. The four largest are Sonali Bank (the largest by branches and total assets among SOCBs), Janata Bank, Agrani Bank, and Rupali Bank. SOCBs are often the banking option in rural and semi-urban areas where private banks have limited presence. They process a significant volume of government salary disbursements, pension payments, and agricultural credit.

Private Commercial Banks (PCBs)

With 43 operating banks, PCBs are the largest and most commercially active segment. They dominate retail banking, digital banking, SME lending, and international transfers. The most prominent names include BRAC Bank, Dutch-Bangla Bank, Eastern Bank (EBL), The City Bank, Mutual Trust Bank, Prime Bank, and Pubali Bank.

Islamic Banks

Bangladesh operates 5 Islamic Shariah-compliant private commercial banks on a profit-loss sharing (PLS) basis rather than interest. Islami Bank Bangladesh Limited (IBBL) is by far the largest , it is the largest private bank in Bangladesh by deposit base and branch count, with 550+ branches. Other major Islamic banks include Al-Arafah Islami Bank and Social Islami Bank. For Muslim savers, IBBL is the dominant choice for both local savings and inward remittances from abroad.

Foreign Commercial Banks (FCBs)

There are 9 FCBs operating as Bangladesh branches of banks incorporated abroad. These serve primarily corporate clients, multinational companies, and high-net-worth individuals. Standard Chartered Bank and HSBC are the two most prominent, both offering trade finance, corporate banking, and premium personal banking services. Citibank N.A. also operates in Bangladesh with a corporate focus.

Specialised Development Banks

Three specialised banks operate with specific mandates: Bangladesh Krishi Bank and Rajshahi Krishi Unnayan Bank for agricultural credit, and Bangladesh Development Bank Ltd. (BDBL) for industrial development. These are not typical retail banking options , they serve targeted economic sectors.

Top Banks in Bangladesh by Category

The leading banks in Bangladesh vary by category , Dutch-Bangla Bank leads on ATM and electronic banking network, IBBL leads on Islamic banking and remittances, BRAC Bank leads on SME lending, and City Bank leads on premium personal banking and international cards.

For everyday retail banking and ATM access: Dutch-Bangla Bank (DBBL) operates the largest electronic banking network in Bangladesh , with more ATM locations than any other bank, with strong coverage outside Dhaka and Chittagong. It is the most practical choice for salaried employees and students who need reliable cash access across the country.

For Islamic and Shariah-compliant banking: IBBL is the largest Islamic bank and the most trusted for halal-compliant savings, deposits, and remittance. Its CellFin app supports international remittance and allows e-KYC account opening.

For SME banking: BRAC Bank is widely recognised as the leading bank for SME lending. It was founded by BRAC, the world's largest NGO, and focuses on small business credit and financial inclusion.

For digital banking and premium personal accounts: The City Bank and Mutual Trust Bank (MTB) are the most cited for digital-first banking in 2026. City Bank offers a Metal Credit Card with lounge access and investment advisory, and has partnered with bKash to offer instant nano-loans. According to The Business Standard, MTB's Neo app won a Best Digital Bank award for 2025/26.

For international and corporate banking: Standard Chartered Bank and HSBC are the top choices for professionals and corporates who need international banking standards and trade finance. Eastern Bank (EBL) is frequently cited as the leading local private bank for international transfer efficiency.

Top Islamic Banks in Bangladesh

Islamic banks in Bangladesh operate under Shariah law, they do not charge or pay interest. Instead, they use profit-sharing structures such as Mudaraba and Musharaka. For Muslim business owners and entrepreneurs, using an Islamic bank ensures all transactions and returns are halal by design.

1. Islami Bank Bangladesh Limited (IBBL) is the largest Islamic bank in Bangladesh by assets and the most widely used by businesses. Its iBanking platform supports BEFTN, NPSB, RTGS, and internal transfers (iTransfer). For 2026, Islami Bank's iBanking platform offers 4 transfer methods with distinct limits and fee structures. iTransfer (Internal) handles same-bank moves between BDT 100 and BDT 10 lakh per day across up to 10 transactions. Same-branch transfers are free; transfers to other IBBL branches cost 0.025% (minimum BDT 5, maximum BDT 100). EFT/BEFTN is the high-volume option, supporting up to BDT 5 lakh per day across 20 transactions at a flat BDT 10 fee.

As of March 2026, unlike more modern systems, Islami Bank iBanking requires you to pre-register every destination account as a beneficiary before you can send a single Taka via EFT or NPSB. Once you add a beneficiary, you often cannot delete them for 20 days, which users criticize as an unnecessary hurdle for one-off payments.

For NRBs: As of March 2026, Islami Bank (IBBPLC) has now expanded its iBanking authentication channels to support Viber and Email as alternatives to traditional SMS, primarily to assist non-resident Bangladeshis (NRBs) who struggle with cellular network delays while abroad or cases where SMS OTP delivery fails. Although users must also check spam folders as email OTP is not always delivered to the primary inbox.

IBBL also operates mCash, the major Bangladeshi MFS to structure accounts under Islamic Mudaraba principles, meaning returns on balance are profit-sharing, not interest, while mCash is structurally Islamic by default, bKash and Nagad now offer competitive Shariah-compliant alternatives within their apps.

2. Sammilito Islami Bank PLC: According to Bangladesh Sangbad Sangstha (BSS) Sammilito Islamic Bank PLC, is a new, Shariah-compliant, state-owned bank formed by the merger of five insolvent Islamic banks (FSIBL, SIBL, EXIM, Union, and Global Islami). It has a capital base of BDT 35,000 crore and operates under the Bank Resolution Ordinance 2025 (which updated the Deposit Protection framework). It is currently under Bangladesh Bank administration as it works to unify the iBanking systems and product lines of the five merged entities.

3. Al-Arafah Islami Bank and Shahjalal Islami Bank are the primary remaining independent, fully licensed scheduled Islamic banks in this tier. They operate under Shariah principles with established SWIFT capabilities for international transfers.

Note that as of April 2026, Social Islami Bank (SIBL) and First Security Islami Bank (FSIBL) no longer exist as independent entities, having been absorbed into Sammilito Islami Bank.

What to know about all Islamic banks for business use:

- All accept inward SWIFT remittances , profit rates rather than interest rates apply to deposit products

- IBBL is the most established for digital banking infrastructure; the others vary significantly in app quality and digital onboarding capability

- For business owners receiving USD from international clients, any Islamic bank with SWIFT capability works as the destination , the Shariah compliance is in the deposit structure, not the wire transfer mechanics

Top State-Owned Banks in Bangladesh

State-owned banks in Bangladesh are government-controlled commercial banks , the largest by branch network and deposit base, but generally slower on digital banking and more documentation-heavy than private banks.

1. Sonali Bank is the largest state-owned bank, but it is no longer the largest bank in Bangladesh overall. It is a fully state-owned commercial bank , not an Islamic bank, despite being listed incorrectly as one in some older sources. Sonali Bank is relevant for businesses that need a wide branch network for cash transactions or government-linked payment flows.

Its digital banking product, Sonali eWallet, has notable friction: Sonali eWallet treats your wallet balance and your linked bank account as two separate silos, and BEFTN draws exclusively from the linked bank account, not the wallet.

If your linked Sonali Bank account has BDT 0 but your wallet holds BDT 10,000, the BEFTN transfer fails. Move funds from wallet to account first using "Wallet to Account," then initiate the transfer. Sonali eWallet also uses a non-standard BEFTN flow that asks you to select a district and branch before the routing number auto-fills , unlike BRAC Bank's Astha or City Bank's CityTouch, which accept a direct 9-digit routing number paste.

2. Janata Bank is the second-largest state-owned commercial bank with a broad branch network and SWIFT capabilities for international transfers. It is used extensively for government payroll, pension disbursements, and corporate salary accounts.

3. Agrani Bank is a state-owned commercial bank , and one of the cheapest destinations for bKash-to-bank transfers. It should be noted that bKash to bank transfer fees actually vary by the receiving bank. Agrani and Sonali charge the least at Tk 10 per Tk 1,000. While City Bank and BRAC Bank charge Tk 11.5 per Tk 1,000. UCB Visa charges Tk 12.5 per Tk 1,000. Hence, the receiving bank determines your bKash-to-bank transfer fee.

4. Rupali Bank is a state-owned scheduled commercial bank with a significant branch network, primarily used for government-linked business transactions and SME lending.

5.Sammilito Islami Bank: Sammilito Islami Bank is a newly established state-owned Shariah-compliant bank formed in 2025 through the merger of five financially distressed Islamic banks as part of Bangladesh Bank’s consolidation strategy to stabilise the banking sector.

It should be noted that as of March 2026, state-owned banks accept inward SWIFT transfers, but their compliance review processes for large or frequent foreign income transfers are generally more documentation-intensive than private banks. For freelancers and businesses receiving regular international income, private banks such as EBL or City Bank are typically faster to process and less likely to require branch visits for verification.

Top Private Commercial Banks in Bangladesh

Private commercial banks offer faster digital onboarding, stronger app-based banking, and more responsive compliance handling for foreign income , making them the preferred choice for most businesses and freelancers receiving international payments.

1. Eastern Bank (EBL) is the most consistently recommended bank by freelancers and remote workers for receiving international income. It offers the EBL Freelancer Suite account , a Foreign Currency (FCY) account for individual freelancers where 35% of income can be held in USD and the remainder credited in BDT , along with a Dual Currency Global debit card for international spending. Community experience shows EBL and its staff are among the most knowledgeable for handling inward SWIFT documentation. City Bank and EBL are named by the community as the most helpful banks for foreign income.

2. City Bank: According to Prothom Alo, City Bank is the first bank currently integrated with Google Wallet for NFC payments in Bangladesh (launched June 2025, expanded to BRAC Bank in February 2026). It is the partner bank behind bKash Pay Later (BDT 500–30,000 loans). City Bank accepts inward SWIFT transfers and has strong digital banking infrastructure via its CityTouch app, which uses a direct 9-digit routing number for BEFTN , no district-branch lookup required.

3. BRAC Bank is the parent company of bKash and one of the most widely used private banks for digital transactions. As of March 2026, BRAC Bank's Astha app provides an instant account number, but the account typically remains in a "view-only" mode, restricting transactions until mandatory backend verification and, often, debit card activation are complete.

While the initial application is immediate, full operational status usually requires 1–2 working days or up to 7 days for manual checks. BRAC Bank accepts a passport as a valid alternative to a utility bill for address verification in digital onboarding. A real BRAC Bank statement documents that small Bangladeshi digital service businesses , web hosts, developers , receive recurring payments directly via bank account-to-account transfer rather than through bKash or Nagad, confirming BRAC Bank works for direct business income flows.

4. Dutch-Bangla Bank (DBBL) operates the Rocket mobile financial service and has the largest ATM network among private banks in Bangladesh. It accepts inward SWIFT transfers and is used for payroll-heavy businesses because Rocket salary disbursement operates as a centralised batch process , DBBL debits the corporate account once and credits all employee accounts simultaneously. Community experience notes DBBL requires NID and utility bill for account opening.

5. Standard Chartered Bangladesh (SCB) offers dedicated foreign income and freelancer account products and is frequently cited alongside EBL for Freelancer Suite-style accounts. When you use an SCB card for international payments, a 3% currency conversion fee is added on non-BDT transactions , this cost reduces the value of international payments made with SCB cards. SCB has strong brand recognition for international business but is more selective in account opening.

Top Banks for Freelancers in Bangladesh

For freelancers specifically , people receiving irregular USD payments from international platforms such as Upwork, Fiverr, Toptal, and Deel , the best bank is the one that handles foreign income documentation without friction, offers a foreign currency account, and processes inward SWIFT transfers quickly.

Ranked by community preference for freelancers:

1. Eastern Bank (EBL) : best overall for freelancers. The EBL Freelancer Suite provides a dedicated FCY account with a 35% USD retention option, a specialised FCY debit card, and staff trained for freelancer income documentation. A Freelancer ID card is generally not mandatory just to receive foreign income into a standard savings account. Banks like Standard Chartered and Eastern Bank (EBL) often list the Freelancer ID as a requirement or a preferred document to open dedicated "Freelancer Suite" accounts, which offer benefits like ERQ (holding USD) and specialised credit cards. An employer appointment letter, contract, or marketplace work order is typically sufficient to satisfy Central Bank "Source of Fund" requirements. However, for large or frequent transfers, banks may still request a Freelancer ID to ensure the funds qualify for government incentives.

2. City Bank: Offers strong digital banking, cooperative for foreign income, and the only bank with Google Wallet NFC integration. No dedicated freelancer product but handles foreign income accounts smoothly.

3. BRAC Bank: Widely accessible with the best mobile onboarding via Astha, but the view-only delay on new accounts can slow down first-use. Good for freelancers who want a bank already connected to bKash for seamless local transfers.

4. Standard Chartered Bangladesh: Offers strong for higher-income freelancers who want a recognised international bank, but the 3% card conversion fee makes SCB cards expensive for international online spending.

What every freelancer should know regardless of bank:

- Freelancers exporting software and IT-enabled services may qualify for a 2.5% government cash incentive on export earnings (Bangladesh Bank FE Circular No. 28, July 2025). Eligibility depends on how the service is classified — consult your bank or Bangladesh Bank for confirmation on your specific service category

- For managing USD before converting to BDT , holding the balance, earning on it, and timing the conversion , a nsave personal USD account covers this layer before the funds ever reach a Bangladeshi bank

How to Open a Bank Account in Bangladesh

To open a bank account in Bangladesh, you need a National Identity Card (NID) or passport, two passport-sized photographs, and a nominee's NID; most private banks now support online or in-app account opening via e-KYC without a branch visit.

Documents required (standard across most banks):

- National Identity Card (NID) or valid passport

- Two passport-sized photographs

- Nominee's NID and photograph

- TIN (Tax Identification Number) , required for some account types and for accounts above certain balance thresholds

In Bangladesh, applying for a personal bank account necessitates providing details regarding the source of funds, a declaration of monthly income, and a specification of resident or non-resident status. Furthermore, if an applicant chooses to use a birth registration or passport as identification in lieu of an NID, they are required to submit information for an introducer.

Major Account types available in Bangladesh include;

- Savings account: Standard interest-bearing account for individuals

- Current account : This is for businesses and high-transaction users; typically no interest but no transaction limits

- Foreign currency (FC) account : This account is able to hold USD, EUR, or GBP without immediate conversion. Although most local banks (like EBL or City) can receive a USD wire transfer into a standard BDT Savings Account. The bank simply converts the USD to BDT at the day's exchange rate before crediting it.You only need an FC or ERQ account if you want to hold the currency as USD to avoid conversion losses or to spend it internationally late

e-KYC digital onboarding

Most major private banks, IBBL (via CellFin), MTB (via Neo), BRAC Bank (via Astha), and City Bank (via CityTouch) , support digital account opening using your NID and a selfie without a branch visit. Before visiting a branch, check whether your chosen bank supports e-KYC opening via their app , this avoids the branch visit entirely for most standard savings account types.

One practical note on digital onboarding at BRAC Bank: As of March 2026, BRAC Bank's Astha app provides an instant account number, but the account typically remains in a "view-only" mode, restricting transactions until mandatory backend verification and, often, debit card activation are complete. While the initial application is immediate, full operational status usually requires 1–2 working days or up to 7 days for manual checks.

Receiving International Transfers Through Bangladeshi Banks

To receive an international wire transfer via SWIFT into a Bangladeshi bank account, provide the sender with your bank's SWIFT code, your account number, and the bank's branch routing information , all major private commercial banks and foreign banks support inward SWIFT transfers.

Most banks apply a currency conversion at the day's interbank rate on arrival , you receive BDT, not USD, unless you hold a foreign currency (FC) account. FC accounts hold USD, EUR, or GBP without immediate conversion and are available at EBL, City Bank, BRAC Bank, and most major PCBs.

Opening an FC account typically requires proof of foreign income source , an employment letter, freelance contract, or marketplace payment record.

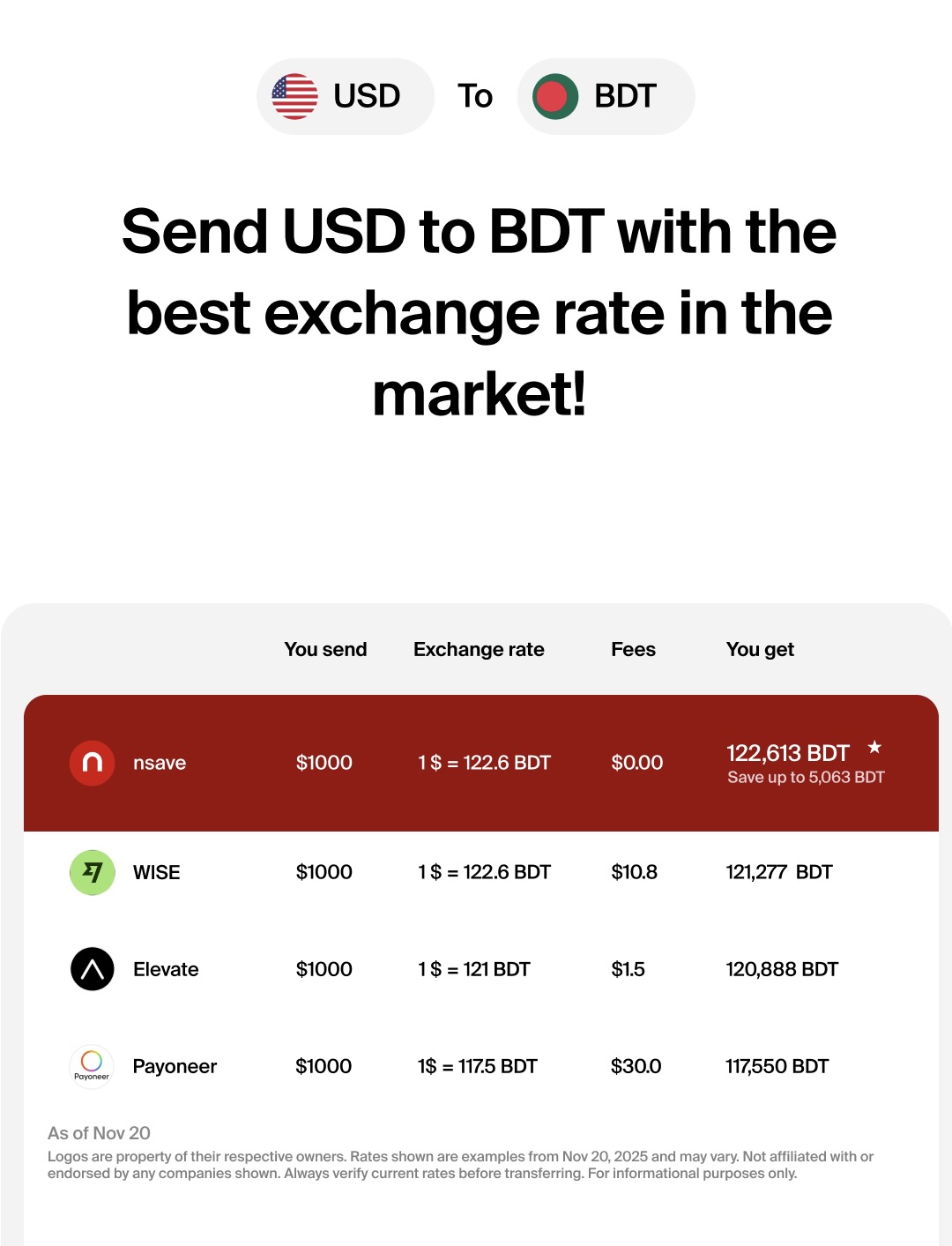

For most Bangladeshis who receive regular USD income from international clients or employers, the local bank is the final destination , not where the USD should sit while it accumulates. The conversion rate on the day of arrival, the transfer fee, and clearing time all affect how much BDT actually lands. Many freelancers and remote workers now use a USD holding account as a layer before converting , giving them rate flexibility and the option to earn on idle balances while they wait.

If you receive USD from international clients , through Upwork, Fiverr, Deel, or a foreign employer , your Bangladeshi bank account is the endpoint, not the starting point. What happens between receiving your USD and converting it to BDT makes a real difference over time. nsave gives you a personal non-resident USD account with ACH receiving details, daily rewards on your balance, and BDT conversion on demand , so your USD isn't sitting idle before you convert.

How to Receive USD and Convert to BDT with nsave

To receive USD from international clients and convert to BDT at a chosen time, open a nsave USD account, share your ACH details as your payout destination, and initiate a BDT withdrawal when you are ready.

Step 1: Open Your nsave USD Account

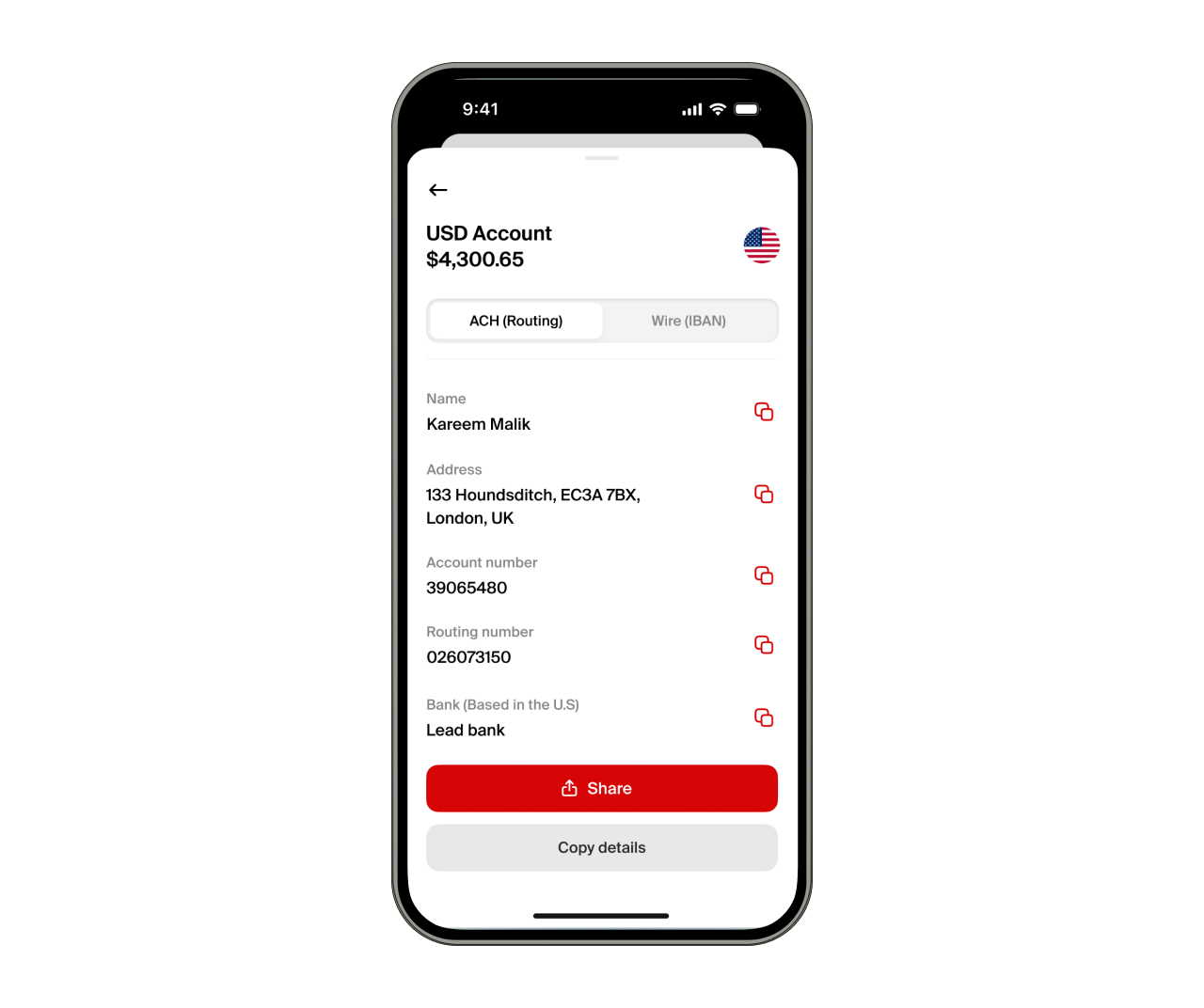

Your nsave account is free on the Standard plan ($0/month). Download the nsave app and complete identity verification using your passport or national ID , usually takes under 10 minutes, no branch visit, no FC account application, no employer letter required. Once verified, nsave assigns a personal ACH routing number and account number

New to nsave? Watch how to set up your account in under 10 minutes:

Step 2: Share Your nsave ACH Details as Your Payout Destination

Any platform that pays to a US account can pay your nsave account directly: Upwork, Fiverr, Toptal, Freelancer.com, PeoplePerHour, Deel, Payoneer, Wise, or a direct client via SWIFT. Receiving USD via ACH or SWIFT is free on both Standard and Pro plans. You give your client or platform your nsave routing number and account number.

Step 3: Convert to BDT and Send to Your Bangladeshi Local Account

To convert USD to BDT, initiate a local currency withdrawal inside the nsave app. The exact BDT amount is shown before you confirm. Minimum transfer fee: $1 (check nsave app as fees may change) and funds arrive in your Bangladeshi local account.

nsave is not a bank. Funds are not FSCS-protecte. nsave is a non-resident USD account for individuals, not a substitute for a full-service Bangladeshi bank account for savings, loans, or government services.

Can I Use Wise to Receive USD Into Bangladesh?

Yes, According to Wise, You can send Bangladeshi Taka (BDT) to bank accounts, bKash, or Nagad, residents cannot open a Wise multi-currency account, order a Wise card, or get USD account details to receive payments directly.

Can I Receive International Payments via Payoneer in Bangladesh?

Yes, Payoneer is widely used by Bangladeshi freelancers on Upwork and Fiverr to receive USD payments, and it supports BDT withdrawals to Bangladeshi bank accounts.

Payoneer charges a currency conversion fee at withdrawal. It does not provide an individually owned US bank account , it provides shared receiving details. The USD sits in your Payoneer balance at 0% until you withdraw, at whatever rate Payoneer applies that day. For freelancers who want to hold USD in a personal account, earn rewards on your balance, and convert to BDT on your own schedule, nsave provides that directly with lower friction.

Key Takeaways

As of April 2026, Bangladesh has 62 scheduled banks divided into four categories: 7 state-owned commercial banks including Sonali Bank and Janata Bank, 43 private commercial banks including BRAC Bank, Dutch-Bangla Bank, City Bank, and Islami Bank Bangladesh, 9 foreign commercial banks including Standard Chartered and HSBC, and 3 specialised development banks. Dutch-Bangla Bank leads on ATM network coverage. IBBL leads on Islamic banking and remittances. BRAC Bank leads on SME lending. City Bank and MTB lead on digital and premium personal banking.

To open a bank account, you need an NID or passport, photographs, and a nominee's NID. Most major private banks support e-KYC digital onboarding without a branch visit, though BRAC Bank's Astha app account activates in view-only mode for 1–7 days before full transactional access. Deposit protection covers BDT 200,000 per depositor under the Deposit Protection Ordinance 2025.

For Bangladeshi freelancers and remote workers who receive USD from abroad, nsave provides a non-resident USD account with ACH receiving details, daily rewards on idle balances (rates vary; see nsave app for current terms), and BDT conversion on demand with a $1 minimum fee (check nsave app as, fees may change) , complementing, not replacing, a local Bangladeshi bank account.

The information in this article is provided for general informational and educational purposes only and does not constitute financial, legal, or tax advice from nsave or any of its affiliates. It is not a substitute for advice from a qualified financial advisor. We make no representations or warranties, whether expressed or implied, that the content is accurate, complete, or up to date.

Fees, exchange rates, incentives, and product availability may change and can vary by user and jurisdiction. Examples are illustrative only. Before making any financial decisions, seek advice from a qualified financial advisor who can assess your individual circumstances and objectives.

nsave helps freelancers and professionals from Bangladesh, Nigeria, Pakistan, Egypt, and beyond receive and manage USD abroad. As a non-bank payment provider, your money is not protected by the Financial Services Compensation Scheme (FSCS).