How to Open a US Business Account in Pakistan

Between 2024 and 2026, several platforms tightened who they accept from Pakistan. Mercury added restrictions, Relay placed Pakistan on its prohibited list, and Wise stopped issuing direct USD account details to owners whose underlying address is in Pakistan.

For founders who want USD, EUR, and GBP business accounts without the US banking approval gauntlet, nsave Business is the most direct option, since any registered company qualifies and no US LLC is required.

For those who specifically need a US-LLC-linked account to connect to Stripe or US payment rails, this guide covers the full route: the LLC and EIN requirements, the real costs, the step-by-step setup, and the one mistake that ends an application permanently.

Do You Need a US LLC to Open a US Business Bank Account?

You need a US-registered LLC with an active EIN for every traditional US business banking platform, including Mercury, Wise Business, Relay, and Airwallex, but you do not need one to hold and move business USD. The distinction matters. US banking rules require a registered legal entity with a US tax identification number before any US business account is activated.

If your real need is receiving USD from clients, paying a team, and converting to PKR, a multi-currency account with a provider such as nsave Business covers that without a US LLC, because it accepts any registered company. If you specifically need a US-LLC-linked account for Stripe or US payment rails, the LLC step cannot be skipped, and the next section walks through it in order.

How to Form a US LLC as a Pakistani Founder

To form a US LLC as a Pakistani founder, you should complete three steps remotely with no US visit required.

1. File the company with a US state

2. Appoint a registered agent

3. Apply for an EIN.

The process is fully online from Pakistan. The one element that controls your timeline is the EIN, because non-residents cannot get it instantly, so treat it as the critical path from day one.

Which State to Form In

Wyoming is the right default for most Pakistani service businesses, agencies, and freelancers. Wyoming offers low cost, strong asset protection, no state income tax, and simple annual compliance. Delaware carries more credibility with US venture investors but costs more and adds a franchise tax. New Mexico has no annual report requirement, making it the cheapest to maintain, though it has the least name recognition.

According to a 2025 LLC University guide on non-resident LLC formation, Wyoming and New Mexico are the two states most often recommended to founders who live outside the US and do not need investor-facing prestige.

LLC Formation Costs

To budget for a Wyoming LLC in year one as a non-resident, plan for the following:

- State filing fee: $100, plus a $3.75 online convenience fee

- Registered agent service: $25 to $300 per year, typically $100 to $125 from a professional provider

- Annual report: $60 per year minimum, due on the first day of the LLC's anniversary month

- Formation service, optional but useful for non-residents: $185 to $297 in year one including EIN guidance

- EIN application: free directly from the IRS

Total year-one cost runs roughly $185 if you do it yourself and around $297 with a professional service. From year two onward, expect about $160 to $250 per year for the registered agent, annual report, and basic compliance.

How to Apply for an EIN as a Non-Resident

To apply for an EIN as a Pakistani founder, file IRS Form SS-4 by fax or mail, because non-residents cannot use the instant online tool. An EIN, the Employer Identification Number, is your company's tax ID, and every US banking platform requires it before opening an account.

According to a 2026 IRS guidance on Form SS-4, applicants without a US tax identification number must submit by fax or post rather than online. Processing takes 4 to 8 weeks by fax and up to three months by post. This is the single biggest timeline blocker for Pakistani founders.

The practical move is to file the EIN the same day you file the LLC, not after the LLC is approved. Some formation services offer expedited non-resident EIN handling, so verify current availability and cost before committing.

Registered Agent and US Business Address

To satisfy both legal and banking requirements, understand that a registered agent address and a business address are two different things. A registered agent is a person or company with a physical US address in your formation state who receives legal documents for the LLC. Every US LLC needs one, and a Pakistani founder cannot serve as their own.

For banking, Mercury and Relay no longer accept the registered agent's address as the LLC's business address, so a separate virtual business address from a service such as iPostal1, Regus, or Anytime Mailbox is now needed for those platforms.

Discussions within Pakistani founder communities through 2025 repeatedly report Wise rejecting applications where only a registered agent address was supplied, since the platform asked for a genuine US business address instead.

Business Account Options for Pakistani Founders (2026)

The fintech accounts most founders reach for first, Mercury, Wise, and Relay, have all tightened their treatment of Pakistani applicants between 2024 and 2026, which means the account that approves you is now the deciding factor rather than its fee card.

The most direct way to hold and move business USD without depending on US banking approval is nsave Business, covered first below. The US-LLC-linked accounts that follow remain viable for founders who specifically need US payment rails, and each entry covers what it gives you, the cost, and the real approval reality.

nsave Business

To hold and move business USD without forming a US LLC, nsave Business gives a registered company multi-currency accounts in USD, EUR, and GBP, accepting any registered entity rather than requiring a US company.

Where Mercury, Wise, and Relay all gate Pakistani founders behind a US LLC, a US business address, or an ITIN, nsave Business removes that gate, because an LLC, a UK Ltd, an agency, or another registered entity all qualify.

The feature set maps to what a Pakistani founder actually does:

- Receive from international clients in USD, EUR, or GBP on any of the three accounts

- Convert to PKR at the available rate

- Pay international employees and contractors in USD or local currency for $0 using bulk payroll via CSV upload

- Pay suppliers and manage expenses from one place

For example, a Lahore SaaS company invoicing two US clients in USD and a German client in EUR can receive all three into separate currency accounts, run monthly contractor payroll by CSV, and convert a portion to PKR, without forming a US entity first.

As a non-bank payment provider, nsave is not a bank, and funds are not FSCS-protected.

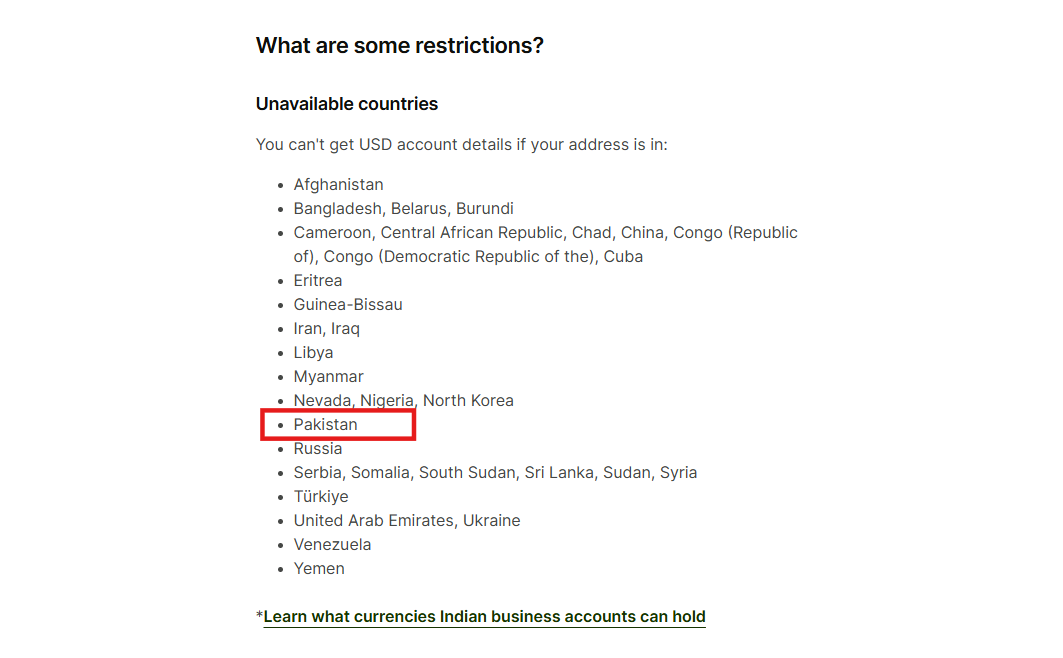

Wise Business

As of June 2026, The Wise Business account functionality is severely limited for locally registered entities and residents within Pakistan. While individuals can easily use Wise to receive cross-border personal remittances directly into their local PKR bank accounts, Wise does not allow users to officially open a fully operational Wise Business account using a local Pakistani business registration. Local residents cannot hold multi-currency balances, generate unique international account details (like USD or GBP routing numbers), or order physical Wise Business debit cards to a Pakistani address.

According to a 2025 Wise Help Centre update on country availability, Pakistan was placed on the list of locations where direct USD account details are not issued if the owner's underlying address remains in Pakistan, which is why the US business address step is decisive here.

To circumvent these strict regional compliance barriers, Pakistani freelancers, startups, and agencies frequently establish foreign business entities, such as a US LLC or a UK LTD, to qualify for a verified Wise Business account. By registering an overseas entity, founders can unlock multi-currency corporate balances and successfully receive foreign client funds.

However, because Wise strictly enforces address verification rules and still won't ship physical corporate cards to Pakistan, many local digital professionals utilize alternative financial platforms like nsave to manage their international business revenues.

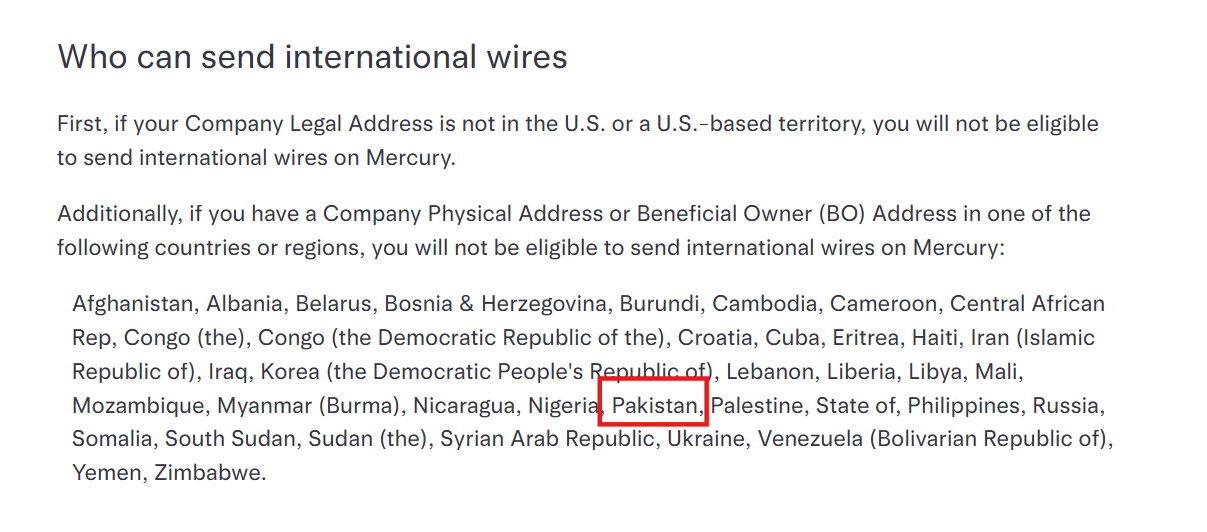

Mercury

As of June 2026, Mercury is completely unavailable for residents, businesses, and beneficial owners based in Pakistan. Following a gradual tightening of its onboarding policies, the U.S.-based fintech platform officially placed Pakistan on its prohibited list, executing a sweeping closure of all remaining Pakistani business accounts.

According to statement disclosures from Mercury's co-founder on X, the platform initially stopped onboarding Pakistani beneficial owners after regional signups suffered from a fraud rate exceeding 10%. Stricter global compliance guidelines and mounting operational strain on partner banks eventually forced the platform to bar any companies maintaining a physical address or significant ownership linked to the country.

Mercury's own co-founder and chief executive, Immad Akhund, who was born in Pakistan, built the company precisely because, at his earlier startups, he consistently struggled with the banks we were forced to use. The irony is sharp for Pakistani applicants, because the same friction that created Mercury now sits between them and it.

This blanket restriction has heavily disrupted the operational flow for Pakistani remote workers, e-commerce sellers, and software startups who previously depended on Mercury to hold corporate USD and process global SWIFT transfers.

Even if a founder establishes a U.S. Delaware LLC, Mercury's strict verification policy blocks international wires and closes accounts if a beneficial owner holding 25% or more of the company resides in Pakistan. Furthermore, physical card delivery to the country is banned. As a result, affected entrepreneurs and freelancers have had to transition to alternative digital platforms like nsave, Payooner and Wise to manage their cross-border business capital.

Relay

As of June 2026, Relay Financial is entirely unavailable for individuals, businesses, and beneficial owners residing in Pakistan. According to Relay's strict regulatory guidelines, Pakistan is officially categorized as a prohibited jurisdiction.

Consequently, the platform will automatically reject any corporate account applications if a beneficial owner holding a significant equity stakeo r anyone acting as a financial controller carries Pakistani citizenship or residency. This strict barrier remains absolute even if an entrepreneur incorporates a legitimate U.S. Delaware or Wyoming LLC, holds an Employer Identification Number (EIN), and maintains a verified corporate mailing address in the United States.

Beyond restrictions on account creation, the platform enforces extensive transactional blockades affecting the region. Relay’s card compliance architecture automatically declines any point-of-sale terminal transactions or online card payments processed by merchants operating inside Pakistan.

Furthermore, the platform prohibits the physical shipping of corporate debit cards to Pakistani addresses, capping issuance exclusively to domestic U.S. destinations.

Due to these structural compliance walls, Pakistani IT exporters, freelancers, and digital startups cannot utilize Relay to store cross-border funds or settle merchant payouts, pushing the regional business ecosystem to rely on more flexible alternative rails like nsave.

Airwallex

Airwallex accepts Pakistani founders who hold a company registered in a supported country, and a US LLC qualifies. It is a multinational fintech offering multi-currency business accounts with local details in USD, GBP, EUR, AUD, and others. Community reports confirm approvals for Pakistani-owned US LLCs.

It supports Stripe and applies low conversion fees. The limits are that it is not FDIC-insured and that it expects an established business with documented activity, so a new company with no trading history may face more questions during review.

Payoneer Business Account

A Payoneer business account does not require a US LLC and provides USD, EUR, and GBP receiving details directly. It is widely used by Pakistani founders receiving payments from Upwork, Fiverr, and Amazon. The trade-offs are a conversion and withdrawal cost on funds and the fact that it is not a full business account, so it cannot connect to Stripe for payment processing. It sits best as a parallel receiving tool.

Traditional US Banks

Chase, Bank of America, and Wells Fargo all require an in-person branch visit for non-resident business accounts, which makes them impractical from Pakistan. Wells Fargo is considered the most accessible of the three for foreign nationals, but the branch visit still applies.

A traditional account makes sense only if you are travelling to the US. If you visit, bring your LLC documents, EIN letter, passport, and US business address documentation. Discussions within Pakistani communities in 2024 note that Capital One and Amex have, in some cases, allowed ITIN-based online onboarding, which is the rare exception to the branch-visit rule.

Platform Comparison for Pakistani Founders

This table consolidates the variables that decide the choice for most Pakistani founders. Treat the approval column as the load-bearing one, since a platform that will not accept you makes its fees irrelevant.

| Platform | Registered entity | Pakistani founder approval | FDIC insured | Stripe Connect | FX fee | Monthly fee |

|---|---|---|---|---|---|---|

| nsave Business | LLC, Ltd, Agencies & Corporate Entities | Built for Pakistan founders | No (Safeguarded) | No | Competitive In-App Rates | See nsave.business |

| Wise Business | US LLC or UK LTD Only | Local PK Address NOT Supported | No (EMI Safeguarded) | Yes | ~0.4% - 0.6% Mid-Market | $0 + Pay-per-transfer |

| Mercury | US LLC Required | Banned (Prohibited List) | Yes (Via Evolve/Choice) | Yes | 1% (0% on USD) | $0 |

| Relay Financial | US LLC Required | Banned (Prohibited List) | Yes, up to $3MVia Sweep Network | Yes | 1% to 2% | $0 (Starter) / $30 (Scale) |

| Airwallex | US or Supported Entity | Not Supported for PK Residents | No (EMI Safeguarded) | Yes | 0.5% to 1.0% | $0 |

| Payoneer Business | Local PK Business or US LLC | High Approval / Widely Used | No (MSB Safeguarded) | No | Up to 2% + Markup | $0 (with activity) / $29.95 yr |

For founders whose priority is receiving and managing business USD without US banking approval, nsave Business is the starting point.

How to Open Your US Business Bank Account Step by Step

Once your LLC is formed and your EIN is in hand, the account opening itself is quick, often 1 to 5 business days for fintech approvals. According to a 2025 Business Globalizer article on non-resident applications, online neobanks typically review a complete application within one to five business days when a clean LLC is established first. The steps below run in sequence.

Step 1: Form Your LLC

To form the company, file Articles of Organization with the Wyoming Secretary of State online at wyobiz.wyo.gov for the $100 state fee plus the $3.75 online convenience fee, with processing usually completing in one business day. Appoint a registered agent at filing, which is required. Prepare an Operating Agreement now, because Wyoming does not require it but banks do.

Step 2: Apply for Your EIN by Fax

To get your EIN, download IRS Form SS-4 from irs.gov, complete it for your LLC, and fax it to the IRS number for international applicant. Do this the same day you file the LLC rather than waiting for approval. Fax processing takes 4 to 8 weeks. If you have heard nothing after four weeks, call the IRS Business Line to confirm receipt.

Step 3: Prepare Your Banking Application Documents

To give yourself the strongest chance of approval, gather a complete document set before you apply, because completeness is the single biggest factor in getting accepted. Most platforms require:

- Articles of Organization, a stamped or certified copy from the state

- EIN confirmation letter from the IRS, the CP 575 or SS-4 fax confirmation

- Operating Agreement, signed and dated

- Passport for all beneficial owners

- A specific business description naming your services, clients, and revenue model

- US business address documentation, such as a virtual office agreement or address verification

Optional additions that strengthen an application include a business website, existing client invoices, or screenshots of platform activity.

Step 4: Submit the Application Once and Correctly

The most important rule in the entire process is that most fintech platforms record a declined application permanently, and a second application from the same LLC is usually auto-rejected without human review. A vague business description is the most common trigger for rejection, so name the services, the clients, and how revenue is generated.

For example, if you run a five-person design agency serving US startups, write that you provide UI and UX design to early-stage US software companies billed through monthly retainers, rather than writing "design services."

Step 5: Activate and Test Your Account

To put the account into service, generate your USD details once approved, send a small test transfer, and link to Stripe if you need it. Set up GBP and EUR receiving details if they fit your payment flows. For Wise Business, the $31 one-time fee activates the USD local account details. From there you can receive ACH and SWIFT transfers and convert between currencies as needed.

Total Cost to Set Up a US LLC and Business Bank Account from Pakistan

To plan the full spend from zero to a live account, the table below combines formation and banking costs into a single first-year and ongoing view.

| Item | One-time cost | Annual recurring |

|---|---|---|

| Wyoming LLC state filing fee | $100 | — |

| Online filing convenience fee | $4.00 | — |

| Registered agent service | $100–$125 (yr 1) | $100–$125 |

| Wyoming annual report (incl. processing) | — | $62 min |

| Operating agreement (DIY) | $0 | — |

| EIN (IRS direct via Form SS-4) | $0 | — |

| Virtual US business address | $10–$30 / mo | $120–$360 / yr |

| Wise Business USD details fee | $31 | $0 |

| Formation service agency fee (optional) | $0–$150 | — |

| Total year one (DIY minimum) | $355–$455 | — |

| Total year one (with service) | $505–$605 | — |

| Ongoing from year two | — | $282–$547 |

Banking fees for conversion and wires are transaction-based and depend on volume. The EIN is free from the IRS, so any service charging more than $30 to $50 for EIN help is charging for the filing work, not the number itself. For founders who choose nsave Business instead, the US LLC formation and ongoing compliance costs above do not apply, since no US entity is required.

Common US Business Banking Problems for Pakistani Founders

Pakistani founders opening a US business account often hit 4 recurring problems, each with a known cause and a fix. Most of these failures trace back to how the application is built and how the account is operated afterward, not to anything wrong with the founder. Here's what goes wrong, why, and what to do about it.

1. Your Application Is Rejected With No Clear Reason

A rejection with no stated reason almost always means your application triggered a manual review and failed it, so you are left to work backward from the 3 most common triggers:

- A vague business description that the reviewer cannot map to a real, operating company.

- A weak or absent web presence that gives the reviewer nothing to verify.

- Pakistani residency, which routes the application into manual review by default.

To clear the review, build the application so a reviewer can confirm the business is real before they ever need to ask. That means doing 3 things first:

- Write a specific business description that names what you sell and to whom.

- Keep an active website live before you apply, not after.

- Attach supporting invoices or signed contracts that show real client activity.

Get these three in place and the manual review stops being a coin flip, because the reviewer now has everything they need to approve you on the first pass.

2. An EIN Delay Blocks Your Account

An EIN delay stalls the whole account, because no US business banking provider will open an account without one. The delay comes down to 2 things working against you:

- Non-residents cannot apply for an EIN online and must submit by fax instead.

- The IRS then takes 4 to 8 weeks to process a faxed application.

To keep that wait off your critical path, treat the EIN as the first task, not the last. Do 2 things:

- Submit the EIN request the same day you form the LLC, so the IRS clock starts immediately.

- Use an expedited filing service if your timeline is tight and the standard 4-to-8-week window will not work.

Start the EIN early and the banking step waits on nothing, which is the difference between launching this month and launching in two.

3. Your Registered Agent Address Is Rejected as the Business Address

The fix is straightforward, obtain a separate virtual business address before you apply. This is a required step now, not an optional one, so building it into your setup from the start saves a rejection and a re-application later.

4. Your Account Is Closed After Opening

An account closed shortly after opening usually means a post-approval compliance review flagged your activity, not your application. The trigger is almost always the operating pattern, specifically a Pakistani login IP, Pakistan-linked transactions, or a jurisdiction review prompted by either. To keep the account open, run it the way a clean, reviewable business runs. Four habits do most of the work:

- Keep a consistent operating pattern rather than sudden, unexplained shifts in activity.

- Never mix personal and business payments through the account.

- Document every transaction so each one has a clear, verifiable purpose.

- Respond promptly to any compliance request, since silence reads as a red flag.

Run the account this way from day one and a compliance review becomes a formality you pass, rather than the moment your access disappears.

What This Makes Possible

A working business USD account changes what a Pakistani founder can realistically build. A few years ago, receiving US client payments, paying an overseas contractor from Karachi, and converting to PKR meant stitching together workarounds that broke without warning. The tighter rules of 2024 to 2026 are real, but they reward preparation rather than blocking it.

Whether through a US LLC paired with a fintech account or through nsave Business with no US entity at all, the same payment infrastructure a US-based company uses is now within reach of a founder working from Lahore or Islamabad. The narrow door is still a door, and walking through it deliberately is what separates the operators who get paid cleanly from the ones still waiting.

The information in this article is provided for general informational and educational purposes only and does not constitute financial, legal, or tax advice from nsave or any of its affiliates. It is not a substitute for advice from a qualified financial adviser. We make no representations or warranties, whether expressed or implied, that the content is accurate, complete, or up to date.

Fees, exchange rates, incentives, and product availability may change and can vary by user and jurisdiction. Examples are illustrative only. Before making any financial decisions, seek advice from a qualified financial adviser who can assess your individual circumstances and objectives.

nsave helps freelancers and professionals from Bangladesh, Nigeria, Pakistan, Egypt, and other emerging markets receive and manage USD abroad. As a non-bank payment provider, your money is not protected by the Financial Services Compensation Scheme (FSCS). Customer funds are held in regulated, UK and EEA financial institutions, separated from company funds, and protected through safeguarding rules designed for electronic money services.